The Ultimate Guide to Private Health Insurance for Self-Employed Professionals

Health insurance for self-employed professionals is critical to protect your finances and health. Without employer-sponsored coverage, you're responsible for finding a plan that fits your needs and budget. Here are the main takeaways:

Why it matters: Medical emergencies can cost tens of thousands of dollars. Marketplace deductibles in 2026 range from $7,500 to $9,000 per person, making private insurance a safer choice for many.

Private plan benefits:

Year-round enrollment.

Nationwide PPO networks for flexibility.

Coverage for pre-existing conditions.

Tax deductions: You can deduct 100% of your premiums from your income.

Cost-saving strategies:

Use High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs) for tax advantages.

Pay out-of-pocket for minor expenses and let your HSA grow tax-free.

How to choose a plan:

Assess your healthcare needs and budget.

Compare premiums, deductibles, and out-of-pocket costs.

Check provider networks to ensure your doctors are covered.

With ACA subsidies expiring and premiums rising by 26% in 2026, private PPO plans are becoming a popular alternative for self-employed professionals. Providers like United National Healthcare offer tailored options with lower deductibles and flexible coverage. Take the time to evaluate your needs, compare plans, and secure coverage that works for you.

Why Self-Employed Workers Need Private Health Insurance

When you're self-employed, you're on your own. There’s no HR team to guide you through plan options, no employer to cover part of the premium, and no built-in safety net if things go sideways. This independence comes with serious financial responsibilities.

Without health insurance, even a single hospital visit can set you back thousands of dollars. In 2026, marketplace deductibles are projected to range between $7,500 and $9,000 per person before coverage kicks in. A sudden medical emergency could wipe out your savings in no time. As Insurance Enterprise USA puts it, “Your health is your business”. Protecting it isn’t just important - it’s essential.

On top of that, income unpredictability makes things even trickier for freelancers and contractors. With earnings fluctuating month to month, estimating your annual income for Marketplace subsidies becomes a challenge. Guess too low, and you might owe money during tax season. Guess too high, and you could miss out on credits that make insurance more affordable. By 2026, even a slight increase in income could push you past the subsidy threshold, potentially tripling your monthly premium. These realities highlight the importance of finding a plan that adapts to your financial situation.

Private health insurance offers a level of flexibility that’s hard to match. Unlike employer-sponsored plans, you can tailor your coverage to suit your needs. Whether you want nationwide PPO access or an HSA-compatible plan to build tax-advantaged savings, private options let you take control. Plus, thanks to the Affordable Care Act, private plans are required to cover pre-existing conditions, ensuring that those with chronic illnesses won’t be left without care.

There’s also a tax benefit: self-employed individuals can deduct 100% of their health insurance premiums from their adjusted gross income. This deduction lowers both income tax and self-employment tax, offering significant savings. Ultimately, private health insurance isn’t just about avoiding financial ruin - it’s about safeguarding your health and ensuring your business thrives. Taking the time to understand these benefits is a crucial step toward protecting both your well-being and your livelihood.

sbb-itb-e9e1681

Main Benefits of Private Health Insurance Plans

Private health insurance plans offer a range of advantages that cater to the specific needs of self-employed professionals and others seeking more control over their healthcare. These benefits go beyond the limitations of employer-sponsored or marketplace options, providing flexibility and tailored solutions for changing circumstances.

Enroll Any Time of Year

One standout feature of many private health insurance plans is the ability to enroll at any time during the year. Unlike marketplace plans, which restrict enrollment to specific periods, private plans often allow you to sign up year-round, with coverage that can start as early as the day after your application is approved. This is especially helpful for those transitioning to freelance work, starting a business, or navigating other life changes without waiting for a qualifying event.

Nationwide PPO Networks

Private PPO plans give you access to a broad network of doctors and specialists across the country. This is a major benefit if you travel frequently or live in multiple states throughout the year. Unlike many marketplace HMO plans that restrict you to in-state providers, PPOs allow you to see specialists without requiring a referral from a primary care physician.

Coverage for Pre-Existing Conditions

If you have a pre-existing condition, ACA-compliant private plans ensure you're covered from day one. However, some TriTerm plans may include a waiting period of up to 12 months for pre-existing conditions. It's important to carefully review the terms of any plan before committing.

Flexible Coverage Options

Private plans are highly customizable, allowing you to adjust your coverage based on your budget and healthcare needs. You can choose from a variety of plan types, including PPO, HMO, EPO, or high-deductible plans that pair with Health Savings Accounts. Some plans even offer first-dollar benefits, which cover routine care immediately, and accident protection that can provide up to $20,000 per incident with only $250 out-of-pocket. This flexibility makes it easier to find a plan that fits your lifestyle and financial goals.

How to Lower Your Health Insurance Costs

If you're self-employed, managing private health insurance costs can feel overwhelming. But with the right tax deductions and plan strategies, you can make these expenses far more manageable. These approaches not only help control out-of-pocket spending but also ensure you’re taking full advantage of the benefits private plans offer.

Deduct 100% of Your Health Insurance Premiums

Self-employed individuals have a significant advantage: the ability to deduct 100% of their health, dental, and vision insurance premiums directly from their income. This deduction is classified as an "above-the-line" adjustment on Schedule 1 of Form 1040, which lowers your Adjusted Gross Income (AGI). The deduction applies to premiums for you, your spouse, your dependents, and even children under 27 - even if they don’t qualify as your tax dependents.

However, there are conditions. You must show a net profit from your business, and you can’t claim the deduction during months when you were eligible for a spouse’s employer-sponsored plan. If you own more than 2% of an S-Corporation, make sure your premiums are included in Box 1 of your W-2 to qualify.

High-Deductible Plans with HSAs

Pairing a High-Deductible Health Plan (HDHP) with a Health Savings Account (HSA) is another smart way to cut costs. This combination offers three key tax advantages: deductions on contributions, tax-free growth, and tax-free withdrawals for qualified expenses. HDHPs often come with monthly premiums that are 20% to 40% lower compared to traditional plans.

"A Health Savings Account represents one of the most powerful tax-advantaged vehicles available to self-employed professionals and 1099 contractors." – Kenny Dennis, CEO & Co-Founder, Uncle Kam

For 2026, contribution limits for HSAs are set at $4,400 for individuals and $8,750 for families. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution. To qualify, your HDHP must have a minimum deductible of $1,700 for individuals or $3,400 for families, with out-of-pocket maximums capped at $8,500 and $17,000, respectively.

Pay for More Healthcare Expenses with Your HSA

HSAs aren’t just for covering insurance deductibles - they can also fund a wide range of medical expenses, including prescriptions, lab fees, dental care, and vision services. Starting in 2026, HSA funds can even be used to pay for Direct Primary Care (DPC) membership fees, capped at $150 per month for individuals or $300 for families. This lets your HDHP handle major medical events while your DPC membership covers routine care.

Another tip? Pay for current healthcare expenses out-of-pocket and let your HSA grow tax-free. The IRS allows you to reimburse yourself years - or even decades - later as long as you’ve saved the receipts. This strategy effectively transforms your HSA into a secondary retirement account. Over a decade, this approach could help you accumulate $15,000 to $30,000 more wealth compared to sticking with traditional insurance.

How to Choose the Right Health Insurance Plan

{Health Insurance Plan Types Comparison for Self-Employed Professionals} :::

Determine Your Healthcare Needs and Budget

The first step in picking the right health insurance plan is understanding your health requirements and financial situation. If you’re generally healthy and only visit the doctor occasionally, a high-deductible plan with lower monthly premiums might be a good fit. However, if you deal with chronic conditions or need regular medications, a plan with higher premiums but lower out-of-pocket costs could save you money in the long run.

Take some time to estimate your expected medical expenses for the year. This includes doctor visits, specialist appointments, and prescriptions. Be sure to check if your medications are included in the plan’s formulary, as insurers often update their covered drug lists.

It’s also important to assess your risk tolerance. Think about how much you can afford to pay monthly versus the deductible and maximum out-of-pocket limits - the total amount you’d need to cover in a worst-case scenario. For 2026, if your Modified Adjusted Gross Income is below $60,240 as a single individual (400% of the Federal Poverty Level), you may still qualify for marketplace subsidies.

"In 2026, health insurance isn't just a personal expense; it's a tax, entity, and cash flow planning challenge." – Condley & Company, L.L.P

By clearly defining your healthcare needs and budget, you’ll be better equipped to compare plans effectively.

Compare Premiums, Deductibles, and Out-of-Pocket Costs

When evaluating plans, don’t just focus on the monthly premium. Add up all potential costs, including deductibles, copays, and coinsurance, to get a clearer picture of your total annual expenses. Consider both routine care and unexpected emergencies when running cost scenarios.

The ACA marketplace organizes plans into metal tiers - Bronze, Silver, Gold, and Platinum - to help you weigh costs and coverage. Bronze plans typically have the lowest premiums but the highest deductibles, making them a good choice if you’re healthy and primarily want coverage for emergencies. Silver plans strike a balance with moderate premiums and deductibles and are the only tier eligible for cost-sharing reductions if your income is between 100%–250% of the federal poverty level. Gold and Platinum plans, while more expensive upfront, offer lower out-of-pocket costs, which can be helpful if you have ongoing medical needs or expensive prescriptions.

Keep in mind that ACA marketplace premiums are projected to rise by about 26% in 2026 as enhanced premium tax credits expire.

"The total cost of coverage is premiums plus out-of-pocket spending, not premiums alone." – Gray Group International

Make sure to align these cost considerations with your healthcare priorities to find a plan that works for you.

Check Provider Networks and Specialist Options

Once you’ve compared costs, it’s time to look at provider networks. Make sure the plan you’re considering includes your preferred doctors, hospitals, and specialists as in-network providers. In-network providers have pre-negotiated rates, which can save you money. Many insurers offer online tools to help you check if your current healthcare providers are covered.

The type of plan you choose also affects how you access specialists. For instance, HMO plans usually require a referral from your primary care doctor to see a specialist, while PPO and POS plans let you visit specialists directly without a referral. If you have a chronic condition that requires frequent specialist visits, a PPO plan might reduce the administrative hassle.

If you travel often or work in different states, look for plans with nationwide coverage or those offering telehealth services. Some plans provide 24/7 virtual care, ensuring you can access medical help wherever you are.

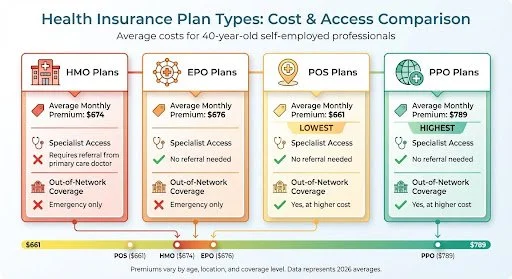

| Plan Type | Average Monthly Premium (40-year-old) | Specialist Access | Out-of-Network Coverage |

|---|---|---|---|

| HMO | $674 | Requires referral | Emergency only |

| EPO | $676 | No referral needed | Emergency only |

| POS | $661 | No referral needed | Yes, at higher cost |

| PPO | $789 | No referral needed | Yes, at higher cost |

What's Included in the Plans

United National Healthcare offers plans specifically designed for self-employed professionals, providing coverage for pre-existing conditions and flexible network access. This means you can choose your preferred doctors and specialists without restrictions.

The plans include key benefits such as preventive care, prescription medications, emergency services, and hospital stays. You can also tailor your coverage to suit your budget - whether that means prioritizing lower premiums or minimizing out-of-pocket costs.

Plan Costs and Coverage Options

The cost of these plans depends on factors like your age, location, and selected coverage level. United National Healthcare uses a metal tier system to make it easier to understand the balance between premiums and out-of-pocket expenses.

| Plan Tier | Coverage Level | Typical Annual Deductible |

|---|---|---|

| Bronze | 60% | $6,000 – $8,000 |

| Silver | 70% | $3,000 – $5,000 |

| Gold | 80% | $1,000 – $3,000 |

| Platinum | 90% | Under $1,000 |

Bronze plans work well if you're in good health and want lower monthly payments.

Platinum plans are better suited for those with ongoing medical needs who prefer predictable costs.

Silver and Gold plans strike a balance, offering moderate premiums and coverage ideal for regular medical care.

This tiered structure makes it easier to find a plan that fits your healthcare needs and financial situation.

How United National Healthcare Helps Self-Employed Workers

United National Healthcare understands how tough it can be for self-employed professionals to manage their own benefits. Jeff Baechle, Senior Director of Products, Employee & Individual at UnitedHealthcare, explains:

"The responsibility for the self-employed individual is that they have to be their own HR manager; they have to figure out what they can afford."

To make this process less overwhelming, United National Healthcare provides personalized guidance and resources. These tools help you compare plans, understand coverage options, and even navigate potential tax benefits. With this kind of support, you can spend less time deciphering insurance details and more time focusing on your business.

How to Apply for Private Health Insurance

Start by gathering the necessary documents. You'll need your personal ID (including your name, date of birth, address, and citizenship status) and income records like 1099 forms, W-2s, and your most recent federal tax return, including Schedule C if applicable.

When applying, you'll need to estimate your net income for the coverage year instead of relying solely on last year's earnings. To calculate this, subtract your business expenses from your revenue. Be prepared to provide a self-employment ledger, which could be a spreadsheet, a printout from accounting software, or even a handwritten record. Include a clear description of your work using straightforward terms like "consultant", "jewelry maker", or "construction."

Next, make a list of your current medications and preferred doctors. Use the plan's formulary tool to check if your prescriptions and healthcare providers are covered in-network. Having this information ready will make the enrollment process smoother.

You can complete your application throughHealthcare.gov, your state exchange, or directly with insurers like United National Healthcare. Typically, if you enroll by the 15th of the month, your coverage will start on the first day of the next month. Keep in mind that Open Enrollment for 2026 runs from November 1, 2025, to January 15, 2026, though some states may extend it to January 31.

Once you’ve chosen a plan, make sure to pay your first premiumpromptly. Setting up autopay can help you avoid missing payments. If you experience a qualifying life event - such as losing other coverage, moving, getting married, or having a child - you may be eligible for a Special Enrollment Period. This gives you 60 days from the event to apply for coverage.

Conclusion

Picking the right health insurance doesn’t have to feel like a daunting task. This guide has given you the tools to make informed decisions - whether it’s about the flexibility of private plans or finding coverage that aligns with your healthcare needs and budget.

There are also some compelling financial perks to consider. For instance, deducting your health insurance premiums from your adjusted gross income can significantly lower your tax bill. Pair that with an HSA, and you’ve got three tax benefits working in your favor. With ACA subsidies set to expire in 2026, many self-employed individuals are turning to private PPO plans to avoid the sharp premium hikes that can result from small income fluctuations.

"Being self-employed means investing in yourself - and nothing is more valuable than your health." – Insurance Enterprise USA

Providers like United National Healthcare offer tailored plans specifically designed for independent workers. These plans often feature lower deductibles - ranging from $3,000 to $7,000 compared to the marketplace’s $7,500–$9,000+ - and give you access to 95% of doctors nationwide. Whether you need coverage for pre-existing conditions or want a plan that evolves with your business, there are solutions to fit your needs.

The key is understanding your priorities and costs. Take the time to compare plans, confirm your doctors and medications are included, and approach your application with confidence. The right health insurance doesn’t just safeguard your well-being - it’s an investment in the future of your career and personal success.

FAQs

How do I estimate income for coverage if my self-employment pay changes each month?

To figure out your income when self-employment pay fluctuates, start by calculating your average monthly income from the past 3 to 6 months.

First, total up all your self-employment earnings for that time frame.

Then, divide the total by the number of months to find your monthly average.

This average provides a steady reference point, making it easier to select health insurance plans and estimate what premiums you can afford.

Which plan type is best if I travel often or need out-of-state doctors?

A private PPO health plan works well for those who travel often or need access to doctors in different states. These plans offer nationwide coverage and more freedom of choice than other types, making them a practical option for self-employed individuals who are frequently on the go.

How do I choose between an HDHP with an HSA and a lower-deductible plan?

When weighing your options, think about your budget and healthcare priorities. A High-Deductible Health Plan (HDHP) with a Health Savings Account (HSA) can be appealing due to its tax perks. Contributions to an HSA are tax-deductible, grow without being taxed, and can be used tax-free for qualified medical costs. However, keep in mind that HDHPs come with higher deductibles, which means you'll face more out-of-pocket expenses before the insurance kicks in.

On the other hand, plans with lower deductibles typically have higher monthly premiums but offer reduced out-of-pocket costs. This can make your healthcare spending more predictable. The best choice depends on how much healthcare you expect to use, your comfort with upfront costs, and whether you prioritize lower premiums or steady, predictable expenses.