Best PPO Health Insurance Plans for 1099 Workers

If you're a 1099 worker - freelancer, contractor, or gig worker - finding the right health insurance can be challenging. PPO plans are a popular choice because they offer flexibility, broad networks, and no referral requirements for specialists. However, they tend to cost more than other options like HMOs. Here’s a quick breakdown of three top PPO plans for 2026:

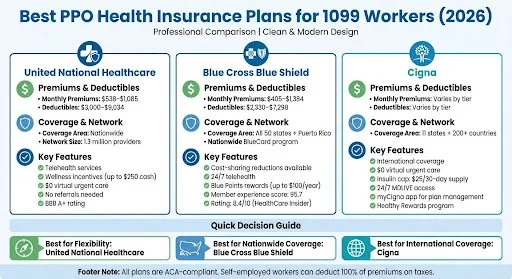

United National Healthcare: Offers flexible pricing tiers (Bronze, Silver, Gold, and Platinum) with premiums ranging from $538 to $1,085/month, depending on the plan. Includes nationwide access to 1.3 million providers, telehealth services, wellness incentives, and deductible options for varying budgets.

Blue Cross Blue Shield (BCBS): Known for its nationwide coverage across all 50 states. Premiums start at $405/month for Bronze plans, with higher-tier plans offering lower deductibles. Includes telehealth, cost-sharing reductions, and wellness rewards.

Cigna: Available in 11 states, with international coverage in over 200 countries. Premiums vary by tier, with features like $0 virtual urgent care, preventive care, and insulin cost caps. Includes tools like the myCigna app for easy plan management.

Quick Comparison

| Provider | Monthly Premiums | Deductibles | Coverage Area | Key Features |

|---|---|---|---|---|

| United National Healthcare | $538–$1,085 | $3,000–$9,034 | Nationwide | Large network, telehealth, wellness incentives |

| Blue Cross Blue Shield | $405–$1,384 | $2,330–$7,298 | Nationwide + Puerto Rico | Nationwide access, cost-sharing reductions |

| Cigna | Varies | Varies | 11 states + global | International coverage, insulin cost caps |

When choosing a plan, consider your budget, healthcare needs, and whether you require nationwide or international coverage. PPO plans are ideal if you value flexibility or frequently travel for work. Don’t forget: as a self-employed worker, you can deduct 100% of your health insurance premiums on your taxes.

Cost (Premiums, Deductibles, Out-of-Pocket Maximums)

United National Healthcare’s Individual PPO Plan offers flexible pricing to suit different budgets. For 2026, premiums are based on the metal tier you choose. Bronze plans range from $538 to $592 per month, with deductibles between $7,950 and $9,034. Gold plans cost around $825 to $841 monthly, with deductibles falling between $6,102 and $7,240. Platinum plans, which come with lower deductibles of about $3,000, are priced at approximately $1,085 per month. Over 50% of ACA members with this plan qualify for $0 monthly premiums thanks to subsidies.

Once you meet your deductible, the plan typically uses an 80/20 or 90/10 coinsurance model until you hit your out-of-pocket maximum. For independent workers keeping a close eye on costs, the plan includes $0 virtual urgent care, $0 preventive care, and generic prescriptions starting at $10 for a one-month supply. You can also earn up to $250 in cash incentives for completing activities like setting up your online account, completing a health risk assessment, or attending your first primary care visit.

Network Coverage (In-Network and Out-of-Network Flexibility)

This plan connects you to a vast network of 1.3 million doctors and 6,700 healthcare facilities across the country. There’s no need to select a primary care physician or get referrals - just book directly with any in-network provider. This flexibility is especially useful if you frequently travel for work or handle gigs in multiple states.

By sticking to in-network providers, you benefit from negotiated rates that lower your deductibles and copayments. While you can visit out-of-network providers, the costs are much higher, as the plan covers a smaller percentage of the charges. You’ll also need to handle claims submissions yourself. For freelancers looking to keep expenses predictable, staying in-network is a smart choice.

Customization Options (Pre-Existing Conditions, Freelancer-Specific Needs)

The plan complies with ACA requirements, meaning your coverage stays intact even if you switch projects, move to a new state, or work remotely. This feature is especially helpful for independent contractors whose work locations or incomes fluctuate. You can also adjust your coverage as your financial situation changes or add supplemental benefits like dental, vision, life, or disability insurance.

Managing the plan is straightforward, thanks to a dedicated online portal and mobile app. These tools allow you to handle claims, billing, and benefits without needing an HR department. Additionally, 24/7 telehealth access ensures you can consult a doctor anytime, which is ideal for those with irregular schedules or limited access to in-person care. United National Healthcare has earned an A+ rating from the Better Business Bureau, and its plan administration receives scores ranging from 86 to 89 points for enrollment and billing support.

Additional Benefits (Telehealth, Wellness Programs)

This plan goes beyond basic medical coverage by focusing on preventive care and virtual services. Most 2026 plans include unlimited virtual urgent care visits at no extra cost, allowing you to consult with doctors from anywhere without disrupting your workday. Preventive services like checkups, screenings, and vaccinations are fully covered even before you meet your deductible.

For freelancers lacking employer-sponsored wellness programs, the plan’s wellness incentives are a big plus. You can earn up to $250 in cash rewards by completing simple tasks like a health risk assessment, setting up your online account, and attending your first primary care visit. These incentives not only encourage healthy habits but also add real value to your coverage.

2. Blue Cross Blue Shield PPO Plan

Cost (Premiums, Deductibles, Out-of-Pocket Maximums)

Blue Cross Blue Shield (BCBS) offers flexible health coverage options tailored to independent workers who need nationwide access and tax advantages. Their plans span all metal tiers, allowing 1099 workers to find coverage that aligns with their budget and healthcare needs. For a 40-year-old self-employed individual in 2026, a Bronze plan costs about $405 per month, with a $7,298 deductible and an $8,679 out-of-pocket maximum. Silver plans, which often include Point of Service benefits with PPO-like flexibility, average $720 per month, featuring a $2,330 deductible and a $6,062 out-of-pocket maximum. At the higher end, Platinum plans cost around $1,384 monthly, with no deductible and a $3,900 out-of-pocket maximum.

For those earning between $15,650 and $62,600 annually in 2026, premium tax credits and full premium deductions can help reduce costs. Additionally, Silver-tier plans may offer cost-sharing reductions to lower deductibles and copays further.

Network Coverage (In-Network and Out-of-Network Flexibility)

BCBS stands out for its nationwide reach, serving all 50 states, Washington D.C., and Puerto Rico. This makes it a great option for freelancers who travel or work across state lines. Through the BlueCard program, members can access care anywhere in the U.S. within the BCBS network. While PPO plans allow visits to out-of-network providers, staying in-network helps keep costs more predictable. To ensure your preferred doctors and facilities are included, use BCBS’s provider search tools.

BCBS scores highly for member experience (95.7) and plan administration (80.5) among POS/PPO insurers, though it has a claim denial rate of about 14%.

Customization Options (Pre-Existing Conditions, Freelancer-Specific Needs)

All BCBS Marketplace plans comply with the Affordable Care Act (ACA), meaning pre-existing conditions are covered without exclusions or higher premiums. These plans cater to the needs of independent workers like gig drivers, consultants, and creatives. If you experience qualifying life events - such as losing job-based coverage, moving, or getting married - you can adjust your plan through Special Enrollment Periods.

For freelancers with fluctuating incomes, updating your income on the Marketplace ensures accurate Advance Premium Tax Credits and helps avoid unexpected tax repayments. Additionally, Bronze and Catastrophic plans are HSA-compatible in 2026, allowing you to save pre-tax dollars for medical expenses.

Additional Benefits (Telehealth, Wellness Programs)

BCBS offers 24/7 telehealth services, giving you access to healthcare professionals anytime. The Blue Points rewards program lets you earn up to $100 in gift cards annually for wellness activities, while the Well onTarget program provides digital tools for health management and preventive care.

BCBS has received high ratings for its self-employed coverage. MoneyGeek gave it a 4.8 out of 5, and HealthCare Insider rated it 8.4 out of 10, calling it the "Best for Nationwide Coverage".

3. Cigna Individual and Family PPO Plan

Cost (Premiums, Deductibles, Out-of-Pocket Maximums)

Cigna's Individual and Family PPO plans are available in 11 states for 2026: Arizona, Colorado, Florida, Georgia, Illinois, Indiana, Mississippi, North Carolina, Tennessee, Texas, and Virginia. These plans align with the Health Insurance Marketplace tiers - Bronze, Silver, Gold, and Platinum - allowing freelancers to choose options that match their healthcare needs and budget.

For those with fluctuating incomes, these plans offer some budget-friendly perks. Virtual urgent care visits cost $0 on most plans, and preventive care is free when you use in-network providers. Prescription drug costs are also manageable, with preferred drugs priced between $0 and $3 on most plans. Additionally, the Patient Assurance Program ensures eligible insulin costs no more than $25 for a 30-day supply. To activate coverage, make your first premium payment immediately after enrollment. This setup is particularly helpful for freelancers balancing variable income streams.

Network Coverage (In-Network and Out-of-Network Flexibility)

Cigna's PPO network offers access to a wide range of doctors and hospitals without requiring referrals or a primary care provider. This flexibility is ideal for freelancers who may need specialized care or frequently travel for work. While out-of-network providers are an option, they come with higher costs and require you to handle claims yourself. Coverage for out-of-network care also involves meeting a separate deductible before benefits kick in.

Emergency and urgent care services are covered at in-network rates, even when provided by out-of-network providers. Plus, Cigna includes 24/7 global emergency coverage. To simplify healthcare management, the myCigna app helps you locate in-network providers and compare costs before scheduling appointments.

Customization Options (Pre-Existing Conditions, Freelancer-Specific Needs)

Cigna designs its plans to address the unique needs of independent workers. All Individual and Family plans comply with the Affordable Care Act, which means pre-existing conditions are fully covered from the first day of enrollment, with no denials, waiting periods, or increased rates. Whether you're managing diabetes, cancer, or another chronic condition, coverage begins immediately. If you're transitioning from another insurance provider, Cigna's Transition of Care feature allows you to temporarily continue treatment with your current providers during the switch.

For freelancers with chronic conditions, plans with higher premiums and lower deductibles may be a better option to keep ongoing care costs predictable. On the other hand, healthier individuals might prefer plans with lower premiums. Additional coverage options, such as dental, vision, Cancer Treatment, and Hospital Indemnity plans, can be added to further tailor the coverage to your needs.

Additional Benefits (Telehealth, Wellness Programs)

Cigna offers 24/7 access to MDLIVE, providing virtual consultations for primary care, dermatology, and behavioral health - perfect for individuals with non-traditional schedules. The Healthy Rewards program adds extra value with discounts on gym memberships, massages, and other wellness services. For more complex medical needs, the My Personal Champion service provides guidance through the healthcare system, while personalized health coaches are available to assist with managing chronic conditions.

Pros and Cons

Breaking down the features of each plan highlights their strengths and trade-offs. United National Healthcare stands out with its personalized coverage options and unrestricted access to specialists. Blue Cross Blue Shield boasts the broadest reach, operating in all 50 states, D.C., and Puerto Rico, alongside a strong HealthCare Insider rating of 8.4/10 and an impressive member experience score of 95.7. Meanwhile, Cigna shines with its international coverage across more than 200 countries, though its U.S. presence is limited to just 11 states.

However, PPO plans tend to come with higher costs. On average, the monthly premium for a PPO plan is $789, about 17% more expensive than HMO plans, which average $674. Blue Cross Blue Shield has a claim denial rate of 14%, while Cigna has faced criticism for increasing premiums, reflected in its satisfaction rating of 4.8/10.

Here’s a table summarizing these points for easy comparison:

| Plan Provider | Monthly Premium | Deductible | Out-of-Pocket Max | Network Availability | Key Strength | Main Drawback |

|---|---|---|---|---|---|---|

| United National Healthcare | Varies | Varies | Varies | Customizable | Flexible provider access with personalized coverage | Pricing varies by location |

| Blue Cross Blue Shield | $720 (POS) | $2,330 | $6,062 | 50 states, D.C., & Puerto Rico | Nationwide access | 14% claim denial rate |

| Cigna | Varies | Varies | Varies | 11 states | Global coverage in 200+ countries | Limited availability in the U.S. |

For frequent travelers, a nationwide network ensures seamless care across the country. If international coverage is a priority, Cigna's global reach is unparalleled. On the other hand, United National Healthcare is ideal for those who value flexibility and freedom from network restrictions. These comparisons enable independent workers to align their healthcare needs with the strengths of each plan.

Conclusion

Finding the right PPO plan as a 1099 worker hinges on several factors: where you work, how often you need care, and what fits your budget. If you travel frequently or work in multiple states, a plan with a strong nationwide network is a smart choice. For example, United National Healthcare stands out for its flexibility, offering personalized coverage and unrestricted specialist access - ideal for those who want more control over their healthcare decisions without being tied to a limited network.

Start by estimating your annual healthcare needs. If you mostly need preventive care, a Bronze plan with lower premiums but a higher deductible might work best. On the other hand, if you have a chronic condition or need frequent care, a plan with higher premiums but lower deductibles could save you money in the long run. Silver plans often strike a good balance for many 1099 workers and are the only tier that offers cost-sharing reductions if your income falls between $15,650 and $62,600 in 2026.

Double-check that your preferred doctors and specialists are included in your plan's network. Out-of-network care can get expensive, even with a PPO. Also, keep an eye on the Maximum Out-of-Pocket limit, which for Marketplace plans in 2026 is capped at $10,600 for individual coverage. This limit can shield you from overwhelming medical expenses. Don’t forget about tax benefits - self-employed workers can deduct 100% of their health insurance premiums on Form 1040, Schedule 1. If you choose a high-deductible Bronze or Catastrophic plan, consider opening a Health Savings Account (HSA) to pay for medical expenses using pre-tax dollars.

Lastly, look into professional group memberships, which can sometimes offer discounted rates that are more affordable than individual marketplace plans. By carefully weighing premiums, deductibles, and your anticipated healthcare needs, you can select a plan that aligns with both your health priorities and your budget.

FAQs

How do I estimate my total yearly cost (premium + deductible + coinsurance) on a PPO plan?

To figure out your total yearly expenses under a PPO plan, you'll need to combine a few key components:

Premiums: Take your monthly premium and multiply it by 12 to get the annual amount.

Deductible: Add the full deductible if you anticipate reaching it during the year.

Coinsurance: Factor in your portion of costs after meeting the deductible. For example, if your coinsurance is 20% and your covered expenses total $3,000, your share would be $600.

Total yearly cost = Premiums + Deductible + Coinsurance. Keep in mind, actual costs can vary depending on how much you use the plan.

What happens if I get care out of network on a PPO plan?

If you get care from a provider outside your PPO network, you'll usually end up paying more. Out-of-network services often mean higher deductibles or coinsurance, and you might even have to handle the claim paperwork yourself. Make sure to review your plan's details so you know the exact costs and steps involved when using out-of-network providers.

How do premium tax credits and the self-employed health insurance deduction work together for 1099 workers?

Premium tax credits and the self-employed health insurance deduction offer 1099 workers a way to lower their taxable income while also qualifying for income-based subsidies. These subsidies can significantly offset healthcare costs, but there's a catch: income-based assistance is set to decrease starting in 2026, which could phase out some of these benefits. By combining these options, you can reduce your total healthcare expenses, but eligibility hinges on your unique income and tax circumstances.