Private Health Insurance in Florida: Your 2026 Guide to Affordable Coverage

Health insurance costs in Florida are rising in 2026, with premiums increasing by an average of 31.5%. Federal subsidy expansions have ended, leading to higher expenses for many households, especially those earning above 400% of the federal poverty level. Here's what you need to know:

Enrollment Periods: Open Enrollment runs from November 1, 2025, to January 15, 2026. Coverage starts January 1 if you enroll by December 15.

Premium Increases: Costs for a 40-year-old in Florida now range from $580/month (Bronze plans) to $764/month (Silver plans).

Plan Types: Choose between HMO, EPO, and PPO plans based on your budget and provider access needs.

Subsidies: Tax credits are available for households earning up to 400% of the federal poverty level. Cost-Sharing Reductions apply to Silver plans for incomes between 100% and 250%.

Special Enrollment: Qualifying life events like job loss or marriage allow you to enroll outside the Open Enrollment period.

To save on healthcare, explore preventive services, consider Health Savings Accounts (HSAs), and compare plans based on total yearly costs. Use HealthCare.gov or consult licensed agents to find the best option for your needs.

2026 Enrollment Periods and Deadlines in Florida

Open Enrollment Period Explained

The Open Enrollment Period for 2026 is scheduled from November 1, 2025, to January 15, 2026. To ensure your coverage starts on January 1, 2026, you must complete your enrollment by December 15, 2025. If you enroll between December 16, 2025, and January 15, 2026, your coverage will begin on February 1, 2026.

This year’s enrollment window is shorter than in previous years, so it’s a good idea to mark your calendar early. Make sure you gather documents like proof of income and details about your current coverage ahead of time. These will help you compare plans and choose one that fits your budget.

Special Enrollment and Qualifying Life Events

Missed the Open Enrollment Period? You might still qualify for coverage through a Special Enrollment Period if you’ve experienced a qualifying life event. These events include losing your insurance, getting married, having or adopting a child, or moving to a different county or state.

When a qualifying life event occurs, you’ll have a 60-day window to enroll. For job-based insurance loss, you can apply up to 60 days before losing coverage to avoid any gaps.

"If you lose your insurance, it's considered a qualifying life event. This means if you lost your health insurance in the past 60 days or if you expect to lose your coverage in the next 60 days, you may qualify for a special enrollment period (SEP)."– UnitedHealthcare

To confirm your eligibility, you’ll need to submit documents like a marriage certificate, birth certificate, or proof of prior coverage. Additionally, American Indians and Alaska Natives can enroll at any time during the year. If you live in a FEMA-designated disaster area or received incorrect information from the Marketplace, you may also qualify for special enrollment.

sbb-itb-e9e1681

Florida's Insurance Marketplace and State Regulations

Understanding Florida's insurance marketplace is essential for making informed decisions, especially after enrollment deadlines have passed.

How Florida's Private Insurance Marketplace Works

Florida uses HealthCare.gov as its Marketplace platform instead of a state-specific exchange. For 2026, 16 private insurance carriers are offering plans, with availability varying by county.

You can enroll in coverage online at HealthCare.gov, through the Marketplace Call Center, or by working with licensed agents. All plans offered through the Marketplace are guaranteed issue, meaning they cover pre-existing conditions without requiring waiting periods.

Marketplace plans are divided into four metal tiers - Bronze, Silver, Gold, and Platinum. These tiers determine how costs are shared between you and the insurer. If your income falls between 100% and 250% of the federal poverty level, you may qualify for additional Cost-Sharing Reductions on Silver plans.

Florida also has strong protections against surprise medical bills. Since 2016, the state has banned surprise balance billing for state-regulated plans. On a broader level, the federal No Surprises Act extends similar protections to self-insured plans. This ensures that in most emergency situations, you won’t face unexpected charges from out-of-network providers.

These details are crucial when choosing a plan and managing healthcare costs effectively. The structure of the Marketplace plays a significant role in how premiums are adjusted, as explained below.

2026 Premium Changes and Rate Trends

Premium costs for 2026 have seen a sharp rise. On average, rates increased by 31.5% across all carriers. This spike is largely due to the expiration of federal subsidy enhancements and the return of the "subsidy cliff" for households earning more than 400% of the Federal Poverty Level.

In October 2025, the Florida Office of Insurance Regulation approved rate changes for all 16 carriers. These changes varied significantly. For example, Sunshine State Health Plan saw a 48.7% increase, while Health First Commercial Plans had the smallest hike at 23.2%.

Your monthly costs will depend on factors like income and age. In Fort Lauderdale, a 40-year-old earning $40,000 annually experienced their lowest-cost plan jump from $34 per month in 2025 to $110 per month in 2026. Older residents above the subsidy threshold faced even steeper increases - a 60-year-old earning $63,000 saw their premium for the lowest-cost plan rise from $191 to $1,064 per month.

| Insurer | 2026 Rate Increase | Plan Types Offered |

|---|---|---|

| Sunshine State Health Plan | 48.7% | HMO |

| Molina Healthcare of Florida | 40.8% | HMO |

| Centene (Ambetter) | 37.9% | HMO, EPO |

| AmeriHealth Caritas | 37.2% | HMO |

| UnitedHealthcare | 29.9% | HMO, PPO |

| Blue Cross Blue Shield of Florida | 29.6% | HMO, PPO |

| Health Options (Florida Blue HMO) | 29.0% | HMO |

| Simply Healthcare Plans (Wellpoint) | 27.2% | HMO |

| Oscar Insurance Company | 26.4% | EPO |

| Florida Health Care Plan | 26.2% | HMO |

| AvMed | 24.5% | HMO |

| Health First Commercial Plans | 23.2% | HMO |

Florida recorded 4,538,772 Marketplace enrollments in 2026, a 4.2% decrease from 2025. These rate increases and enrollment trends highlight the importance of carefully comparing providers and understanding what drives your costs before choosing a plan.

How to Find Affordable Private Coverage

Navigating private insurance options in 2026 means understanding how plans are structured and what financial aid might be available. With an average rate hike of 31.5% across carriers, choosing wisely is more important than ever.

Your household income plays a big role in determining costs, including eligibility for Premium Tax Credits and the amount you receive. Other factors, like age and location, also influence pricing. For instance, a 64-year-old could pay up to three times more than a 21-year-old for the same coverage, and rates can vary significantly depending on your county or zip code.

To make an informed decision, focus on total yearly costs instead of just the monthly premium. Add up your annual premiums (after any subsidies) and estimate your out-of-pocket expenses based on how often you visit doctors or need prescriptions.

Metal Tiers and Plan Types Explained

Marketplace plans are categorized into four tiers: Bronze, Silver, Gold, and Platinum. These tiers define how costs are split between you and the insurer but don't reflect the quality of care.

Bronze plans: Lowest monthly premiums but highest deductibles and out-of-pocket costs. For example, a 40-year-old in Florida pays about $580 monthly for a Bronze HMO. These plans work well if you rarely need medical care but want protection against major expenses.

Silver plans: Moderate premiums and out-of-pocket costs, averaging $764 per month for a 40-year-old. Silver plans are the most popular because they strike a balance between affordability and coverage. They're also the only tier eligible for Cost-Sharing Reductions (CSRs) if your income falls between 100% and 250% of the federal poverty level.

Gold plans: Higher premiums, averaging $770 per month, but lower costs when you need care. These plans are ideal if you have chronic conditions, require regular prescriptions, or need frequent specialist visits.

Platinum plans: The highest premiums at around $1,248 per month but with the lowest out-of-pocket costs. These plans are best for those expecting major medical expenses or requiring extensive care.

"The 'best' plan isn't the one with the lowest premium, but the one that provides the most predictable and manageable costs for your specific health and financial needs." – Pounds Health Insurance

Income-Based Subsidies and Tax Credits

If you purchase coverage through HealthCare.gov, Advance Premium Tax Credits can lower your monthly insurance bill. However, 2026 marks a shift as federal subsidy enhancements from 2025 have expired, reinstating the "subsidy cliff".

For households earning above 400% of the federal poverty level, premium assistance is generally unavailable. This threshold is $60,240 annually ($5,020 monthly) for an individual and $124,800 annually ($10,400 monthly) for a family of four.

Cost-Sharing Reductions (CSRs) are separate from premium subsidies and apply only to Silver plans. If your income is between 100% and 250% of the federal poverty level, CSRs can lower deductibles, copayments, and coinsurance. In early 2025, two-thirds of Marketplace enrollees in Florida benefited from CSRs.

Your eligibility depends on your Modified Adjusted Gross Income (MAGI), which includes wages, self-employment income, unemployment benefits, and taxable Social Security income. If your income changes - due to a raise, job loss, or other event - report it promptly to avoid owing back excess tax credits.

"If you qualify for CSR, a Silver plan often beats Bronze on total yearly cost - even when Bronze has the lower monthly premium." – Blake Insurance Group

Provider Networks and Pre-Existing Conditions

Marketplace plans are required to cover pre-existing conditions without waiting periods or higher premiums based on your health history. However, provider networks vary widely between plans, so it's crucial to check if your doctors, specialists, and preferred hospitals are included. This is especially important for HMO and EPO plans, which usually don't cover out-of-network care except in emergencies.

In Florida's 2026 Marketplace, HMO plans dominate due to their lower premiums. For example:

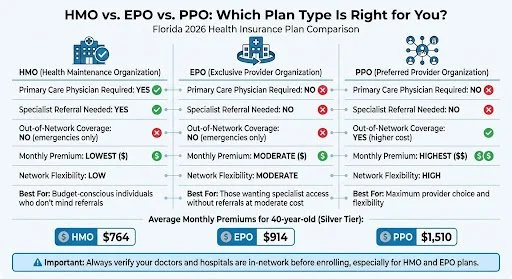

Average Silver HMO: $764/month

Average Silver EPO: $914/month

Average Silver PPO: $1,510/month

These price differences reflect network restrictions. HMOs typically require referrals for specialists and limit coverage to in-network providers.

Also, confirm your prescriptions are covered under the plan's formulary. Coverage can vary even within the same metal tier. Contact the insurer directly or use their online provider directory to verify drug coverage before enrolling.

Understanding these network and coverage details is essential before comparing the next set of plan features.

What to Compare When Choosing a Private Plan

Florida Health Insurance Plan Types Comparison 2026: HMO vs EPO vs PPO

Once you understand metal tiers and income-based subsidies, the next step is comparing plan structures. The goal? Finding the right balance between provider access and your total annual costs. For 2026, Florida’s Marketplace includes 16 carriers offering HMO, EPO, and PPO plans - each with its own pros and cons.

When choosing a plan, plan type plays a big role in determining how you access care. It affects whether you need referrals, which doctors you can visit, and what you’ll pay for out-of-network services. Beyond just monthly premiums, you’ll also need to factor in deductibles, copayments, coinsurance, and the out-of-pocket maximum to get a full picture of your annual costs. With premiums expected to rise sharply in 2026, comparing plan types carefully can help you align your healthcare needs with your budget.

HMO vs. PPO vs. EPO Plans

HMO, EPO, and PPO plans each offer different levels of provider access and cost-sharing. Here’s how they stack up:

HMO (Health Maintenance Organization): These plans require you to choose a Primary Care Physician (PCP) who manages your care and provides referrals for specialists. You’re limited to in-network providers (except in emergencies), but HMOs typically have the lowest monthly premiums.

EPO (Exclusive Provider Organization): EPO plans have gained popularity in Florida because they don’t require PCP referrals. You can see specialists directly, but coverage is still limited to in-network providers outside of emergencies. Many individual plans in Florida for 2026 are EPOs, offering a middle ground between affordability and flexibility.

PPO (Preferred Provider Organization): PPO plans offer the most freedom - you can visit any provider without referrals and even get partial coverage for out-of-network care. However, this flexibility comes with the highest monthly premiums.

Here’s a quick comparison of the key features:

| Feature | HMO | EPO | PPO |

|---|---|---|---|

| Primary Care Physician Required | Yes | No | No |

| Specialist Referral Needed | Yes | No | No |

| Out-of-Network Coverage | No (emergencies only) | No (emergencies only) | Yes (higher cost) |

| Monthly Premium | Lowest | Moderate | Highest |

| Network Flexibility | Low | Moderate | High |

Since Florida’s provider networks change annually, it’s essential to confirm that your preferred doctors, specialists, and hospitals are in-network for 2026. This step is especially important for HMO and EPO plans, as using out-of-network providers means covering the entire cost yourself.

Next, let’s look at how to weigh monthly premiums against out-of-pocket costs.

Balancing Monthly Premiums and Out-of-Pocket Costs

With Florida’s average premium rates set to rise by 31.5% in 2026, deciding between lower monthly premiums and lower usage costs depends on your medical needs.

If you’re generally healthy and don’t visit doctors often, a plan with lower monthly premiums and higher deductibles might save you money. You’ll pay less each month while still being covered for major emergencies.

If you have chronic conditions or frequent medical needs, plans with higher monthly premiums but lower out-of-pocket costs are likely a better fit. Silver or Gold plans often reduce costs for specialist visits, prescriptions, and diagnostic tests, which can lower your total annual spending despite the higher monthly payments.

To estimate your total yearly cost, add your annual premiums (after subsidies) to your expected out-of-pocket expenses. Consider doctor visits, prescriptions, and any planned medical procedures. Also, make sure your ongoing prescriptions are covered at reasonable costs. This step ensures your plan meets both your medical and financial needs.

United National Healthcare's Personalized Florida Plans

Cost (Premiums, Deductibles, Out-of-Pocket Maximums)

Blue Cross Blue Shield (BCBS) offers flexible health coverage options tailored to independent workers who need nationwide access and tax advantages. Their plans span all metal tiers, allowing 1099 workers to find coverage that aligns with their budget and healthcare needs. For a 40-year-old self-employed individual in 2026, a Bronze plan costs about $405 per month, with a $7,298 deductible and an $8,679 out-of-pocket maximum. Silver plans, which often include Point of Service benefits with PPO-like flexibility, average $720 per month, featuring a $2,330 deductible and a $6,062 out-of-pocket maximum. At the higher end, Platinum plans cost around $1,384 monthly, with no deductible and a $3,900 out-of-pocket maximum.

For those earning between $15,650 and $62,600 annually in 2026, premium tax credits and full premium deductions can help reduce costs. Additionally, Silver-tier plans may offer cost-sharing reductions to lower deductibles and copays further.

Network Coverage (In-Network and Out-of-Network Flexibility)

BCBS stands out for its nationwide reach, serving all 50 states, Washington D.C., and Puerto Rico. This makes it a great option for freelancers who travel or work across state lines. Through the BlueCard program, members can access care anywhere in the U.S. within the BCBS network. While PPO plans allow visits to out-of-network providers, staying in-network helps keep costs more predictable. To ensure your preferred doctors and facilities are included, use BCBS’s provider search tools.

BCBS scores highly for member experience (95.7) and plan administration (80.5) among POS/PPO insurers, though it has a claim denial rate of about 14%.

Customization Options (Pre-Existing Conditions, Freelancer-Specific Needs)

All BCBS Marketplace plans comply with the Affordable Care Act (ACA), meaning pre-existing conditions are covered without exclusions or higher premiums. These plans cater to the needs of independent workers like gig drivers, consultants, and creatives. If you experience qualifying life events - such as losing job-based coverage, moving, or getting married - you can adjust your plan through Special Enrollment Periods.

For freelancers with fluctuating incomes, updating your income on the Marketplace ensures accurate Advance Premium Tax Credits and helps avoid unexpected tax repayments. Additionally, Bronze and Catastrophic plans are HSA-compatible in 2026, allowing you to save pre-tax dollars for medical expenses.

Additional Benefits (Telehealth, Wellness Programs)

BCBS offers 24/7 telehealth services, giving you access to healthcare professionals anytime. The Blue Points rewards program lets you earn up to $100 in gift cards annually for wellness activities, while the Well onTarget program provides digital tools for health management and preventive care.

BCBS has received high ratings for its self-employed coverage. MoneyGeek gave it a 4.8 out of 5, and HealthCare Insider rated it 8.4 out of 10, calling it the "Best for Nationwide Coverage".

3. Cigna Individual and Family PPO Plan

Cost (Premiums, Deductibles, Out-of-Pocket Maximums)

Cigna's Individual and Family PPO plans are available in 11 states for 2026: Arizona, Colorado, Florida, Georgia, Illinois, Indiana, Mississippi, North Carolina, Tennessee, Texas, and Virginia. These plans align with the Health Insurance Marketplace tiers - Bronze, Silver, Gold, and Platinum - allowing freelancers to choose options that match their healthcare needs and budget.

For those with fluctuating incomes, these plans offer some budget-friendly perks. Virtual urgent care visits cost $0 on most plans, and preventive care is free when you use in-network providers. Prescription drug costs are also manageable, with preferred drugs priced between $0 and $3 on most plans. Additionally, the Patient Assurance Program ensures eligible insulin costs no more than $25 for a 30-day supply. To activate coverage, make your first premium payment immediately after enrollment. This setup is particularly helpful for freelancers balancing variable income streams.

Network Coverage (In-Network and Out-of-Network Flexibility)

Cigna's PPO network offers access to a wide range of doctors and hospitals without requiring referrals or a primary care provider. This flexibility is ideal for freelancers who may need specialized care or frequently travel for work. While out-of-network providers are an option, they come with higher costs and require you to handle claims yourself. Coverage for out-of-network care also involves meeting a separate deductible before benefits kick in.

Emergency and urgent care services are covered at in-network rates, even when provided by out-of-network providers. Plus, Cigna includes 24/7 global emergency coverage. To simplify healthcare management, the myCigna app helps you locate in-network providers and compare costs before scheduling appointments.

Customization Options (Pre-Existing Conditions, Freelancer-Specific Needs)

Cigna designs its plans to address the unique needs of independent workers. All Individual and Family plans comply with the Affordable Care Act, which means pre-existing conditions are fully covered from the first day of enrollment, with no denials, waiting periods, or increased rates. Whether you're managing diabetes, cancer, or another chronic condition, coverage begins immediately. If you're transitioning from another insurance provider, Cigna's Transition of Care feature allows you to temporarily continue treatment with your current providers during the switch.

For freelancers with chronic conditions, plans with higher premiums and lower deductibles may be a better option to keep ongoing care costs predictable. On the other hand, healthier individuals might prefer plans with lower premiums. Additional coverage options, such as dental, vision, Cancer Treatment, and Hospital Indemnity plans, can be added to further tailor the coverage to your needs.

Additional Benefits (Telehealth, Wellness Programs)

Cigna offers 24/7 access to MDLIVE, providing virtual consultations for primary care, dermatology, and behavioral health - perfect for individuals with non-traditional schedules. The Healthy Rewards program adds extra value with discounts on gym memberships, massages, and other wellness services. For more complex medical needs, the My Personal Champion service provides guidance through the healthcare system, while personalized health coaches are available to assist with managing chronic conditions.

Pros and Cons

Breaking down the features of each plan highlights their strengths and trade-offs. United National Healthcare stands out with its personalized coverage options and unrestricted access to specialists. Blue Cross Blue Shield boasts the broadest reach, operating in all 50 states, D.C., and Puerto Rico, alongside a strong HealthCare Insider rating of 8.4/10 and an impressive member experience score of 95.7. Meanwhile, Cigna shines with its international coverage across more than 200 countries, though its U.S. presence is limited to just 11 states.

However, PPO plans tend to come with higher costs. On average, the monthly premium for a PPO plan is $789, about 17% more expensive than HMO plans, which average $674. Blue Cross Blue Shield has a claim denial rate of 14%, while Cigna has faced criticism for increasing premiums, reflected in its satisfaction rating of 4.8/10.

Here’s a table summarizing these points for easy comparison:

| Plan Provider | Monthly Premium | Deductible | Out-of-Pocket Max | Network Availability | Key Strength | Main Drawback |

|---|---|---|---|---|---|---|

| United National Healthcare | Varies | Varies | Varies | Customizable | Flexible provider access with personalized coverage | Pricing varies by location |

| Blue Cross Blue Shield | $720 (POS) | $2,330 | $6,062 | 50 states, D.C., & Puerto Rico | Nationwide access | 14% claim denial rate |

| Cigna | Varies | Varies | Varies | 11 states | Global coverage in 200+ countries | Limited availability in the U.S. |

United National Healthcare makes navigating Florida's health insurance landscape easier with plans tailored to fit your unique needs. Whether you're self-employed, managing a chronic condition, or seeking a budget-friendly option for 2026, there's something designed for you.

Flexible Coverage for Any Budget

United National Healthcare offers plans for individuals, families, freelancers, and small businesses in counties like Miami-Dade, Broward, Palm Beach, Hillsborough, Orange, and Leon. With an average statewide rate increase of 31.5%, finding the right balance between affordability and coverage is more important than ever. Plans are available in Bronze, Silver, and Gold tiers, allowing you to decide how to manage your monthly premiums versus out-of-pocket costs. Whether you need basic emergency care or more extensive coverage for ongoing medical needs, these plans are adaptable to your budget and healthcare requirements. Plus, network restrictions are removed, giving you even more flexibility.

Plans Without Network Limits and Pre-Existing Condition Coverage

United National Healthcare provides plans that do away with network limits, ensuring you have access to over 55,000 pharmacies across Florida. Many plans also include no-cost virtual urgent care and primary care visits. Preventive services like annual checkups, flu shots, and mammograms are covered without any out-of-pocket expenses. Members can even earn up to $250 in rewards for completing simple activities such as setting up an online account, completing a health risk assessment, or visiting a primary care provider. Additionally, through December 31, 2026, members receive a 20% discount on Walgreens brand health and wellness products.

Help with Applications and Learning Resources

United National Healthcare simplifies the enrollment process with its digital tools. Use uhcexchange.com to search for plans and enroll, and myuhc.com/exchange to manage benefits and locate network providers. Educational resources, including glossaries and guides, help clarify insurance terms and explain the differences between Bronze, Silver, and Gold plans. Before applying, you can verify eligibility by entering your county and income details online. This step helps determine if you qualify for Premium Tax Credits or Cost-Sharing Reductions. Don’t forget to make your binder payment (your first month’s premium) to activate your 2026 plan. These tools and resources make securing the right plan quick and straightforward.

Ways to Reduce Healthcare Costs in 2026

With Florida facing an average rate hike of 31.5% for 2026, finding ways to cut healthcare expenses is more important than ever. Your health plan includes benefits designed to help you save money while maintaining access to essential care.

Using Preventive Care and Included Benefits

Preventive care services - like annual physicals and vital screenings - are covered by private health insurance at no extra cost. These services are a smart way to avoid expensive treatments down the road.

"Early detection makes treatment easier and less costly." - ClearMedica

For example, catching high blood pressure during a routine, no-cost checkup can help you sidestep the hefty bills that come with advanced medical care. Scheduling these visits early in the year ensures you’re taking full advantage of these benefits.

Additionally, if you’re enrolled in a Silver-tier plan, you may qualify for cost-sharing reductions. These can lower your deductibles, copayments, and coinsurance, giving you another way to manage out-of-pocket expenses.

Health Savings Accounts and Flexible Spending Accounts

Tax-advantaged accounts like Health Savings Accounts (HSAs) are another effective tool for reducing healthcare costs. HSAs allow you to pay for medical expenses - such as deductibles, copayments, and even some dental or vision costs - using pre-tax dollars. This not only lowers your taxable income but also helps stretch your healthcare budget. Plus, unused HSA funds roll over annually and earn tax-free interest.

"By using untaxed dollars in a Health Savings Account (HSA) to pay for deductibles, copayments, coinsurance, and some other expenses, you may be able to lower your overall health care costs." - HealthCare.gov

To use an HSA, you’ll need a High Deductible Health Plan (HDHP). Starting in 2026, all Bronze and Catastrophic plans in the Florida Marketplace will be HSA-compatible, giving you more choices. For instance, Bronze plans - averaging around $580 per month for a 40-year-old in Florida - offer a budget-friendly way to unlock HSA benefits. While Catastrophic plans have lower premiums, they don’t qualify for premium tax credits like Bronze plans do. Carefully compare premiums, tax credit eligibility, and potential HSA savings to find the plan that aligns with your financial goals.

Finding Affordable Health Insurance in Florida for 2026

Balancing your healthcare needs with your budget starts by evaluating how often you visit the doctor, the medications you take, and any upcoming procedures. This helps you choose the right coverage level. For example, average monthly premiums in Florida for a 40-year-old are $580 for Bronze plans and $764 for Silver plans.

Once you've assessed your health needs, check if you're eligible for financial assistance to reduce costs. Subsidies can significantly lower premiums, and for households earning between 100% and 250% of the federal poverty level, choosing a Silver-tier plan provides Cost-Sharing Reductions. These reductions help lower deductibles and copays, making healthcare more affordable.

To compare options, visit HealthCare.gov. Make sure the plans you're considering include your preferred doctors and facilities in their network. Keep in mind that in Florida, out-of-network care often requires you to pay the full cost upfront. When comparing plans, look beyond just the monthly premium - factor in the maximum out-of-pocket costs to avoid surprises.

For expert help, companies like United National Healthcare offer tailored Florida health plans with flexible coverage options. They also provide free assistance through licensed agents who can guide you through subsidy applications and help navigate complex provider networks, ensuring your plan fits both your needs and budget.

In 2026, 4,538,772 Floridians have already enrolled in Marketplace plans. While premiums have risen by an average of 31.5%, taking the time to explore all available options and leveraging subsidies can make quality health insurance more accessible.

FAQs

How do I estimate my total yearly cost (premium plus out-of-pocket) before picking a plan?

To figure out your total yearly cost, add up your annual premium and any expected out-of-pocket expenses, such as deductibles, coinsurance, and copayments. Tools like the Florida Health Insurance Cost Calculator can help. Simply input your income to get an estimated monthly premium, then multiply that amount by 12 to calculate the yearly total. Be sure to review the plan details and any subsidies available to fine-tune your estimate based on your specific healthcare needs and usage habits.

What should I do if my income changes after I enroll so I don’t owe money back at tax time?

If your income changes after you've signed up for a health plan, it's important to update your information right away with the Marketplace or your insurance provider. This helps make sure your subsidies are adjusted correctly, so you’re not hit with unexpected tax bills later. Starting with the 2026 rules, repayment caps on excess subsidies were removed, meaning you could owe money if changes aren’t reported. Keep records of your updated income and report any changes promptly through the appropriate portal.

How can I confirm my doctors, hospitals, and prescriptions are in-network before I sign up?

To make sure your doctors, hospitals, and prescriptions are covered, start by checking the insurer's provider directory or using their online search tools. It's also a good idea to contact your healthcare providers directly to confirm they accept the plan. For prescriptions, review the plan's formulary to see if your medications and pharmacy are included. Doing this ahead of time helps ensure your preferred providers and prescriptions are part of the plan.