Network-Free Coverage for Freelancers

Freelancers often struggle with health insurance due to the limitations of network-based plans. These plans restrict access to specific providers, creating challenges for those who travel or work in multiple locations. Network-free health insurance solves this problem by allowing you to see any licensed provider without worrying about networks, referrals, or geographic restrictions.

Here’s why network-free plans are a great option for freelancers:

No network restrictions: Visit any licensed doctor or specialist nationwide.

Simplified billing: No surprise fees for out-of-network care.

Flexibility for travel: Consistent coverage, even if you work in different cities.

Customizable plans: Choose coverage levels (Bronze, Silver, Gold, Platinum) based on your needs and budget.

Affordable options: Monthly premiums can be as low as $200 with subsidies.

United National Healthcare offers network-free plans tailored for freelancers, providing personalized options to fit varying healthcare needs and income levels. Whether you need basic coverage or comprehensive care, these plans simplify health insurance for independent workers.

Key takeaway: Network-free health insurance eliminates the hassles of traditional plans, giving freelancers the freedom to access care wherever they are.

What Is Network-Free Health Insurance?

Network-Free vs Traditional Health Insurance Plans Comparison for Freelancers

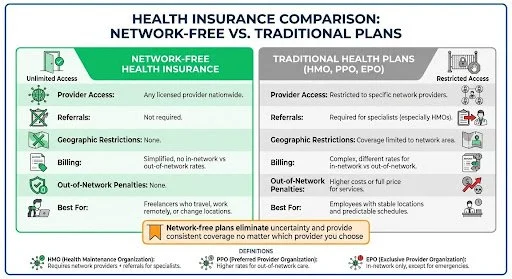

Network-free health insurance allows you to visit any licensed healthcare provider without worrying about network restrictions. Unlike traditional plans, there are no penalties for choosing one doctor over another. For freelancers, whose lives often involve constant change, this type of coverage provides much-needed flexibility. Let’s dive into how this model works and why it’s particularly beneficial for freelancers.

Traditional health insurance plans - like HMOs, PPOs, EPOs, and POS plans - require you to stick to specific provider networks. As Definitive Healthcare explains:

A health insurance network is a group of doctors and other healthcare providers built by insurance companies to provide medical care for their members and help them save money.

The downside? If you want to see a provider outside the network, you’re often hit with full costs or surprise fees.

Network-free health insurance eliminates these restrictions. You get the same level of coverage no matter which licensed provider you choose. That means no referrals for specialists, no geographic limitations, and a much simpler billing process. For freelancers who travel frequently, work remotely, or simply value the freedom to pick their own doctors, this setup is a game-changer.

Main Features of Network-Free Plans

The standout feature of network-free health insurance is complete freedom to choose your provider. You can visit any licensed doctor, specialist, or facility across the country without needing a referral or worrying about whether they’re in-network.

This also simplifies billing since there’s no distinction between in-network and out-of-network rates. For freelancers who split their time between cities or are always on the go, nationwide access is a major plus. These plans also cut down on the administrative headaches that often come with traditional insurance, making healthcare more straightforward and accessible.

Network-Free vs. Traditional Health Plans

Traditional health insurance plans rely on networks to manage costs, but this often limits your options. For example, HMOs require you to stick to network providers and usually mandate referrals for specialists. PPOs offer more flexibility but charge higher rates for out-of-network care, while EPOs typically cover only in-network services unless it’s an emergency. As Lyndsey West from Renown Health points out:

Seeing an in-network provider for medical services can significantly reduce your medical expenses.

The catch? You save money only if you stay within the network. If you need or prefer to see a provider outside that network, you’re likely to face steep out-of-pocket costs or unexpected charges.

Network-free plans remove this uncertainty. They provide consistent coverage no matter which provider you choose, making it easier to plan and budget for healthcare expenses. This is especially important as insurers increasingly lean toward narrow-network plans to control costs. By prioritizing access and choice over network-based cost savings, network-free insurance offers a critical advantage for freelancers juggling unpredictable schedules and locations.

Why Freelancers Need Network-Free Coverage

Freelancing comes with plenty of perks - freedom, flexibility, and the ability to work from just about anywhere. But when it comes to healthcare, freelancers face unique hurdles. Traditional insurance plans are built for employees with stable schedules and fixed locations, not for individuals who are constantly on the move.

Network-based insurance often complicates access to care. Picture a graphic designer who splits time between New York and Miami, a consultant traveling across the country, or a writer working remotely from different cities. For them, network-based plans can create barriers to getting the care they need. That’s where network-free coverage steps in, offering the same level of care no matter where you are or which doctor you choose. Let’s break down why this matters.

Problems Freelancers Face with Traditional Insurance

Traditional insurance plans come with geographic restrictions and unexpected costs. For example, if your HMO or EPO coverage is based in Colorado, but you’re spending a few months working in Texas, you’re essentially uninsured for routine care. Any non-emergency visits outside your network mean paying full price, which defeats the purpose of having insurance.

Even plans with out-of-network options, like PPOs, can sting your wallet. While they offer some coverage for out-of-network providers, the rates are significantly higher. For freelancers already paying an average of $500 per month for health insurance, these surprise costs can be financially overwhelming. On top of that, managing referrals, navigating claim denials, and keeping track of in-network providers can feel like a full-time job.

Another major headache is the lack of portability. If you move to a new city for a project or relocate to be closer to clients, switching plans often becomes necessary. This means starting over with new deductibles, finding new providers, and dealing with potential gaps in coverage. Network-free plans eliminate these hassles by offering seamless portability.

How Network-Free Plans Provide Flexibility

Network-free plans are designed with freelancers in mind. They let you see any licensed provider in any state without worrying about networks, referrals, or surprise bills. Whether you’re traveling for work or relocating, your coverage stays consistent, giving you one less thing to worry about.

This kind of flexibility is especially valuable for freelancers juggling clients in multiple cities or working on short-term projects in different locations. Instead of wasting time researching provider networks every time you travel, you can focus on finding the best doctor for your needs. Billing is simple, coverage is reliable, and you avoid the stress of dealing with network restrictions while meeting client deadlines.

For eligible freelancers, network-free plans through United National Healthcare can lower monthly premiums to as little as $200. By estimating your net self-employment income for the coverage year instead of relying on last year’s earnings, you may also qualify for subsidies that make these plans even more affordable.

Customizing Network-Free Health Insurance with United National Healthcare

Network-free health insurance gives you the power to shape your plan around your specific needs and budget. Unlike traditional employer-based plans that often take a one-size-fits-all approach, these customizable options let you prioritize what matters most to you - whether that's lower monthly premiums, predictable out-of-pocket costs, or coverage that accommodates pre-existing conditions.

How to Create a Personalized Plan

The first step is understanding your healthcare usage over the past year. Take note of how often you visited doctors, consulted specialists, or filled prescriptions. If your healthcare needs are minimal, a Bronze plan might be the way to go. These plans typically have lower monthly premiums, ranging between $538 and $592, but come with higher annual deductibles - about $7,950 to $9,034. You'll save on your monthly payments but will face higher costs if significant care is needed.

For those who require regular medical attention, a Gold plan or Platinum plan could be a smarter choice. Gold plans cost around $825 to $841 per month with deductibles between $6,102 and $7,240, while Platinum plans come in at $1,085 monthly with a much lower deductible of $3,000. These options provide more predictable expenses, making them ideal for frequent healthcare users.

If you go with a high-deductible plan, consider pairing it with a Health Savings Account (HSA). HSAs offer a triple tax advantage: your contributions lower taxable income, the funds grow tax-free, and withdrawals for qualified medical expenses aren't taxed. For freelancers or anyone with fluctuating income, this can act as both a financial safety net and a tax-saving tool.

These flexible options highlight how United National Healthcare simplifies the customization process, making it easier to tailor your health insurance to your unique situation.

United National Healthcare Plan Features

United National Healthcare takes the flexibility of network-free plans to the next level, offering features that make managing your healthcare straightforward and adaptable. Their approach allows you to choose your preferred metal tier (Bronze, Silver, Gold, or Platinum), add optional benefits like dental or vision coverage, and adjust your plan each year based on changes in your health or income.

One standout feature is the inclusion of coverage for pre-existing conditions. This means you won’t face higher rates or denials based on your medical history. Combined with the ability to tweak your plan annually, this ensures you have a healthcare solution that grows and adapts with you.

Costs and Features of Network-Free Plans

United National Healthcare's network-free plans provide access to 1.3 million providers nationwide with straightforward pricing. You can choose a metal tier based on your healthcare needs. For example, Bronze plans range from $538 to $592 per month with deductibles between $7,950 and $9,034. On the other hand, Platinum plans cost about $1,085 per month and come with a $3,000 deductible. These plans are designed to simplify billing, avoiding the unexpected costs often associated with out-of-network care.

One standout feature is the elimination of surprise charges for out-of-network care. This makes them especially appealing for frequent travelers or those living in multiple states. However, it’s important to review and adjust your plan annually to ensure it continues to meet your needs as your circumstances change.

For freelancers with fluctuating incomes, premium tax credits could significantly reduce costs. Starting in 2026, those who qualify might pay as little as $50 per month, though eligibility will be capped at 400% of the federal poverty level. This change follows the expiration of enhanced subsidies from 2021–2025.

Advantages and Disadvantages of Network-Free Plans

The primary benefit of these plans is freedom of choice. You’re free to visit any doctor, specialist, or pharmacy without worrying about network restrictions. This is a huge plus for freelancers who frequently relocate or work remotely from various locations.

| Feature | Advantage | Limitation |

|---|---|---|

| Flexibility | Nationwide access with no penalties | Premiums may vary based on customization |

| Customizability | Adjustable deductibles and add-ons | Requires active management |

| Transparency | Clear costs and fewer hidden charges | May feel unfamiliar to some users |

However, these plans do require more effort on your part. You’ll need to assess your healthcare needs, compare metal tiers, and decide which optional benefits work best for you. If you prefer a simple, hands-off approach, the annual review process might feel like an inconvenience. But for freelancers who value control and flexibility, the ability to customize their healthcare often outweighs the extra effort.

Next, find out how to apply and tailor your network-free coverage with United National Healthcare for a hassle-free experience.

How to Apply for Network-Free Coverage with United National Healthcare

Application Process Steps

Start by evaluating your healthcare needs. Take a close look at your medical history, ongoing prescriptions, and any upcoming procedures or specialist visits. This will help you choose the plan that aligns best with your situation. If you regularly take medications, jot down their names and monthly costs to pinpoint the coverage that fits.

Then, request a quote by providing your personal details and information about any dependents. If you're applying outside the regular Open Enrollment period, you'll need to show proof of a qualifying life event, like getting married, having a baby, moving to a new state, or losing prior coverage.

Work with United National Healthcare during the customization phase to tweak deductibles, add optional benefits, and confirm there are no network restrictions. They’ll help you select the appropriate metal tier and consider extras like dental or vision coverage.

Finally, complete your application by submitting required information, including your Social Security Number and date of birth. If you're self-employed, estimate your income for the upcoming year to determine eligibility for premium tax credits. Health policy expert Jenny Chumbley Hogue explains:

If you're self-employed, one of the hardest parts of the marketplace is that in November, you've got to determine your income for the next year.

Getting this estimate right is crucial to avoid repaying subsidies later.

Application Tips and Best Practices

Gather all necessary documents ahead of time, including your medication list and income records. If you’re adding dependents, make sure you have their details ready too. Keep in mind that around 4 out of 5 applicants qualify for financial help through premium tax credits, so accurate income reporting is key.

If you have a doctor you rely on, double-check their participation. As Hogue advises:

If you have a doctor who is critical to your happiness, call the office and ask, 'Do you take any marketplace plans?' Don't rely on the doctor's website; do not rely on the insurance company's website.

Even with plans that don't restrict networks, confirming your doctor’s acceptance of your insurance can save you from unexpected issues.

When consulting with United National Healthcare, ask specific questions about plan flexibility. For example, clarify how the "no network restriction" feature works in real-world scenarios. If your income varies throughout the year - common for freelancers or seasonal workers - discuss how to adjust your plan to reflect those changes.

Following this process ensures you're well-prepared to manage your coverage and make adjustments when needed.

Maintaining and Adjusting Your Coverage

Keeping your health coverage up-to-date is crucial for freelancers. It ensures your network-free plan stays aligned with your changing needs.

Annual Plan Reviews and Updates

Mark your calendar: Open Enrollment runs from November 1 to January 15. This is your yearly chance to evaluate whether your current plan still fits your situation. As Jenny Chumbley Hogue puts it:

If you haven't looked at health insurance options in a while, it may be time to take a look again.

Freelancers should make it a habit to review their plans annually, especially if there have been changes in income, family size, or healthcare needs. These factors can influence your premium tax credits and the plan tier that works best for you. To simplify the decision, consider using a three-scenario model (low, medium, and high usage) to determine which tier offers the best balance of cost and coverage.

Before you renew, take a moment to confirm directly with your doctor that they still accept your plan. If the process feels overwhelming, don’t hesitate to consult an experienced insurance agent or broker for guidance.

Adding Supplemental Coverage Options

Beyond yearly reviews, supplemental coverage can provide extra protection for both your health and finances.

For those with high-deductible plans (like a Bronze-tier plan), consider pairing it with additional coverage. At the same time, maximize contributions to your Health Savings Account (HSA). By 2026, individuals will be able to contribute up to $4,300 in pre-tax dollars, offering significant tax advantages.

If you’re working with United National Healthcare, ask how adding supplemental coverage could impact your deductibles and out-of-pocket maximums. This step can help you make informed decisions about extra coverage options that fit your budget and needs.

Conclusion

Freelancing offers the freedom to work on your terms, but it also means taking charge of essentials like health insurance. Network-free health insurance can give you the flexibility that traditional plans often lack. You get to pick your doctors, avoid referrals, and stay covered no matter where your work takes you. While these plans tend to cost about 17% more than HMO options, they provide the adaptability many freelancers need to manage their healthcare.

United National Healthcare is a go-to resource for freelancers looking to build tailored health plans. Whether you opt for a Bronze plan at $538 per month for basic coverage or a Platinum plan at $1,085 per month for more frequent care, they help you find the right fit. On top of that, they offer ongoing support, helping you review and adjust your plan as your needs evolve. This hands-on approach ensures your coverage grows with you.

Staying on top of your health insurance is crucial. Make it a habit to review your plan during Open Enrollment, adjust coverage as your circumstances change, and explore options like Health Savings Accounts (HSAs) for tax benefits. With a little planning, you can maintain strong healthcare coverage while enjoying the independence that freelancing brings.

FAQs

-

Whether your doctor accepts a network-free plan largely depends on the provider. For instance, United National Healthcare offers plans with nationwide PPO networks. These plans typically allow you to visit any doctor who agrees to accept the plan, even if they aren’t within a specific network. However, it’s always a good idea to check directly with your doctor to make sure they accept the plan.

-

If your health insurance plan allows you to see specialists without requiring a network, you usually don’t need referrals. However, this depends on the specific details of your plan and provider. Make sure to check the terms of your policy to see if referrals are required.

-

Health insurance subsidies in the U.S. hinge on your Modified Adjusted Gross Income (MAGI), which factors in your self-employment income after deductions. For freelancers, MAGI begins with your net self-employment income, then subtracts expenses and deductions such as self-employment taxes, health insurance premiums, and retirement contributions. By reducing your MAGI, you might qualify for subsidies like premium tax credits, which can help lower the cost of marketplace health plans if your income falls within the eligibility thresholds.