Health Insurance for Real Estate Teams

Finding health insurance as a real estate professional can be tricky. Most agents are independent contractors, meaning they don’t get employer-sponsored benefits. Without proper coverage, a medical emergency could cost months of income. At the same time, offering benefits to contractors can create legal risks for brokerages.

Here’s what you need to know:

1099 Contractors: Independent agents usually rely on individual health plans. These plans are flexible and portable but often cost more.

W-2 Employees: Small brokerages with employees can opt for group health plans, which spread costs and may qualify for tax credits.

Coverage Gaps: Fluctuating income and limited provider networks make standard plans less ideal for agents.

New Options: Programs like United Real Estate Group’s Healthcare save agents an average of $10,000 annually compared to open-market plans.

The right plan depends on your team’s structure and needs. Whether you’re a solo agent or managing a hybrid team, balancing cost, coverage, and compliance is key.

Insurance Needs for Real Estate Teams

Independent Contractors vs. Small Business Teams

The structure of your real estate team plays a big role in determining your insurance options. Most real estate agents operate as 1099 independent contractors, which means they typically miss out on traditional employer-sponsored health insurance. Instead, they often turn to the individual marketplace, where premiums tend to be higher compared to group insurance rates.

On the other hand, brokerages that employ W-2 administrative staff or function as small businesses may qualify for small group health plans. These plans often come with broader provider networks and better cost-sharing arrangements. Plus, brokerages with fewer than 25 employees might be eligible for a health care tax credit covering up to 50% of premium costs through the Small Business Health Options Program (SHOP).

For hybrid teams - those combining W-2 employees with 1099 contractors - offering health benefits can get tricky. Providing benefits to independent contractors requires careful planning to ensure compliance with worker classification rules. Many brokerages address this by using voluntary group arrangements, which allow contractors to access group-style rates without changing their employment classification.

These distinctions in employment structure highlight the unique challenges real estate professionals face when it comes to securing the right insurance coverage.

Coverage Gaps in Standard Insurance Plans

Beyond these structural differences, real estate professionals often encounter specific gaps in coverage that standard insurance plans don’t address. For example, fluctuating income can complicate subsidy eligibility on the ACA marketplace. An agent might earn high commissions one year, only to find themselves priced out of affordable coverage options the next. Plans designed for salaried workers often fail to account for the unpredictable nature of commission-based income.

Another common issue is limited provider networks, which can be a major headache for agents who travel frequently for showings or client meetings. Many marketplace plans restrict coverage to specific geographic areas, leaving agents without in-network options when they work outside their home region. For example, group vision insurance for National Association of Realtors (NAR) members starts at just $12.70/month, but individual plans are often more expensive and come with narrower networks and fewer benefits.

These challenges underline the importance of carefully evaluating insurance options to ensure they meet the unique needs of real estate professionals.

Health Insurance Options for Real Estate Teams

Real estate professionals have two main choices for health insurance: group health plans and individual health insurance plans. Each caters to different team setups and offers unique benefits. Let’s break down how these options meet the needs of real estate teams.

Group Health Plans for Real Estate Agencies

For brokerages with W-2 employees, small business group health plans are a solid option. These plans spread premium costs across the team, often making them more affordable than individual marketplace rates. They typically include perks like PPO coverage, as well as dental, vision, and supplemental insurance.

Group plans work best for teams with 2 to 50 employees, offering savings through group-negotiated rates. Most of these plans come with tiered networks - such as HMO, PPO, or EPO - which influence both care options and costs. Additionally, group plans address the challenge of coverage gaps, a common concern for professionals with fluctuating incomes.

Individual Health Insurance Plans

For independent agents or 1099 contractors, individual health insurance plans provide unmatched flexibility. Companies like United National Healthcare specialize in tailoring these plans to fit your health and financial needs.

Individual plans come with benefits like no network restrictions and portable coverage, meaning your insurance stays with you even if you switch brokerages. They also cover pre-existing conditions without exclusions, ensuring ongoing medical needs are met. While these plans may have higher premiums since risk isn’t shared, they are fully tax deductible, offering financial relief for self-employed agents managing their own expenses.

What to Consider When Choosing Health Insurance

Selecting health insurance involves juggling costs and access to care, which can be especially tricky for real estate professionals. With unpredictable income, 1099 contractor status, and varying team setups, finding the right plan becomes even more important.

Balancing Cost and Coverage

It's all about finding the sweet spot between monthly premiums and out-of-pocket expenses. High-deductible plans might seem appealing with their lower monthly costs, but they require you to pay more upfront before benefits kick in. On the flip side, low-deductible plans come with higher premiums but offer more predictable costs when you actually need care.

Think about how often you use healthcare. If you're generally healthy and don't visit doctors often, a high-deductible plan paired with a Health Savings Account (HSA) could help you save money while building tax-advantaged savings. But if you or your family members need regular medical care, take medications, or see specialists, a low-deductible plan might save you from surprise expenses.

Don't overlook network accessibility. Make sure your preferred doctors and facilities are in-network. Out-of-network care can quickly wipe out any premium savings you thought you had.

For team leaders working with 1099 contractors, offering voluntary coverage options rather than requiring participation can help maintain independent contractor status while still providing support.

Tax benefits and compliance with regulations are also key factors to keep in mind when choosing a plan.

Tax Benefits and ACA Compliance

If you're running a small brokerage with W-2 employees, take a look at the Small Business Health Options Program (SHOP). Teams with fewer than 25 employees could qualify for a health care tax credit that covers up to 50% of premium costs. This can significantly reduce the expense of group insurance.

Independent agents have options too. The self-employed health insurance deduction can lower taxable income, and team leaders might be able to deduct premium contributions for their W-2 employees as ordinary business expenses. These tax perks can make offering or securing comprehensive coverage more affordable.

Don't forget about ACA compliance. To avoid penalties, plans must meet minimum coverage standards and include essential health benefits like preventive care, prescription drugs, and emergency services. Plus, plans can't charge more based on health status, which is a big plus for older agents or those with pre-existing conditions.

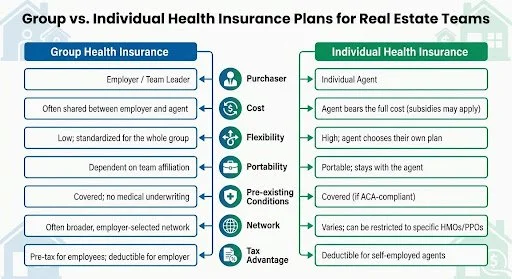

Group vs. Individual Health Plans

Group vs Individual Health Insurance Plans for Real Estate Teams Comparison

When deciding between group and individual health insurance plans, the best choice often depends on the structure of your real estate team. Brokerages with W-2 employees typically lean toward group plans. These are purchased by a team leader and tend to offer lower per-person premiums and broader provider networks. However, one major drawback is that this coverage is tied to your team. If an agent leaves, they lose their insurance.

On the other hand, individual plans provide a different kind of flexibility. These are purchased directly by agents and remain with them regardless of their brokerage or employment status. This portability is a critical advantage for real estate agents, who often switch brokerages or work independently. While individual plans might come with higher premiums, agents who qualify for subsidies can receive financial assistance to help make these plans more affordable.

Comparison Table: Group vs. Individual Plans

| Feature | Group Health Insurance | Individual Health Insurance |

|---|---|---|

| Primary Purchaser | Employer / Team Leader | Individual Agent |

| Cost Responsibility | Often shared between employer and agent | Agent bears the full cost (subsidies may apply) |

| Flexibility | Low; standardized for the whole group | High; agent chooses their own plan |

| Portability | Dependent on team affiliation | Portable; stays with the agent |

| Pre-existing Conditions | Covered; no medical underwriting | Covered (if ACA-compliant) |

| Network Restrictions | Often broader, employer-selected network | Varies; can be restricted to specific HMOs/PPOs |

| Tax Advantage | Pre-tax for employees; deductible for employer | Deductible for self-employed agents |

This side-by-side comparison highlights how each type of plan caters to different needs, making it easier for real estate teams to determine which option works best for their structure and priorities.

How to Enroll with United National Healthcare

Now that you've clarified your plan selection, let’s walk through the process of enrolling with United National Healthcare.

The enrollment process is simple, but a little preparation goes a long way. Make sure you have your Tax ID Number, business legal name, and current contact information ready before you start. Having these details on hand will help speed up the application process.

Enrollment Timelines and Options

The timeline for enrollment depends on your team structure and the type of plan you choose. For those setting up a group health plan for W-2 employees, enrollment periods are often scheduled in the fall, allowing coverage to begin on January 1st. Processing applications generally takes 14 to 45 days, but in some cases, it could take up to 60 days.

Missed the open enrollment window? You might still qualify for a Special Enrollment Period if you’ve experienced a qualifying life event like marriage, the birth of a child, or the loss of other health coverage. If you don’t qualify, short-term health insurance is available to cover gaps, with options lasting from one month to nearly a year.

Tools to Simplify the Process

United National Healthcare provides tools to make the enrollment process more transparent. TheOnboard Pro Tool allows you to track your application in real time. Once your application is submitted, you’ll receive a reference number for immediate confirmation. This feature is particularly helpful for real estate teams, as it allows you to plan coverage start dates and manage budgets effectively.

Enrollment for Solo Agents and Independent Contractors

If you’re a solo agent or independent contractor, individual plans offer year-round enrollment options, giving you the flexibility to secure coverage whenever it works best for you. To apply, you’ll need to provide your age, location, the level of coverage you’re looking for, and your estimated net self-employment income if you’re applying for subsidies.

Taking the time to enroll efficiently ensures you’ll have coverage tailored to meet the unique demands of your real estate work.

Conclusion

Choosing the right health insurance for your real estate team doesn’t have to be complicated. Whether you’re managing W-2 employees or collaborating with independent contractors, the goal is to find a plan that balances cost-effectiveness with solid coverage.

United National Healthcare simplifies the process of navigating insurance options for both 1099 contractors and W-2 employees. Their licensed agents help you leverage NAR benefits and select plans that align with your team’s needs. This guidance can enhance recruitment efforts, improve retention, and streamline operations.

Offering the right insurance can make your team more competitive. With United National Healthcare, you can create benefits that attract top talent while maintaining compliance for independent contractors. Options include individual plans with tax-deductible premiums or small business group plans for teams of 2–50, all managed through user-friendly digital tools like online portals and mobile apps.

Reach out to United National Healthcare’s licensed agents to explore costs, group options, enrollment, and subsidy details. They’ll help you design insurance solutions that support your team’s success in the fast-paced real estate industry.

FAQs

-

If your team includes 1099 agents, providing group health benefits can be tricky. According to IRS rules, group health plans are restricted to W-2 employees, and offering such benefits to independent contractors could risk misclassification.

That said, there are still ways to support your 1099 agents. You might consider offering stipends to help them cover health-related expenses, adjusting their compensation to account for the lack of benefits, or pointing them toward individual health insurance options available through the marketplace. These steps can show your team you value their well-being without violating regulations.

-

Group health insurance plans are often a smarter choice for real estate teams. They not only help attract and keep top talent but also provide broader coverage at potentially lower costs per person. While individual plans might suit independent contractors, group plans tend to be more budget-friendly and better aligned with the needs of a team. This makes them a practical option for building loyalty and managing benefits effectively.

-

To sign up with United National Healthcare, you'll generally need to provide proof of identity, licensing, certifications, and in some cases, proof of insurance or other relevant credentials.

The timing of enrollment varies. If it's during the Open Enrollment Period (typically November 1 to January 15), the process is straightforward. However, if you're applying during a Special Enrollment Period, you'll likely need to submit documentation for a qualifying life event, such as a job change or marriage. Keep in mind, verifying eligibility for special enrollment can take a few weeks.