How to Get Health Insurance After Losing Your Job

Losing your job doesn’t just mean a loss of income - it often means losing your health insurance too. Here’s how to quickly secure new coverage to avoid gaps in protection:

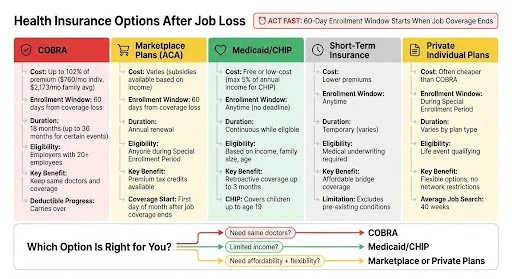

COBRA: Continue your current plan, but expect higher costs (up to 102% of the premium).

Marketplace Plans: Apply within 60 days of losing coverage; subsidies may lower costs based on your income.

Medicaid/CHIP: Free or low-cost options for those with limited income; enroll anytime.

Short-Term Insurance: Temporary coverage, but limited benefits and exclusions.

Private Plans: Flexible options, often cheaper than COBRA, but vary in coverage.

Act fast - your 60-day window for Marketplace or COBRA enrollment starts when your job-based coverage ends. Assess your healthcare needs, budget, and eligibility to choose the best option.

Health Insurance Options After Job Loss: Costs, Eligibility, and Coverage Comparison

Step 1: Review Your Situation and Coverage Needs

Step 1 is all about laying the groundwork for selecting the right replacement coverage. This starts with verifying your insurance timeline and understanding your personal healthcare priorities.

Check Your Current Insurance Status

First, confirm the exact termination date of your employer-based insurance. The best way to do this is by reaching out to your HR department or benefits administrator. Additionally, contact your insurance company to double-check your policy status and find out if any grace periods apply. Don’t make assumptions - your confirmed termination date determines when your new coverage needs to begin and starts the clock on your 60-day enrollment window.

Ask your employer for a "loss of coverage" notice. This document officially states when your insurance ends, and you’ll likely need it when applying for a Marketplace plan.

Keep in mind that most Marketplace plans will kick in on the first day of the month following your coverage termination.

Once you’ve nailed down your coverage end date, you’re ready to evaluate your healthcare needs and financial situation.

Determine Your Healthcare Needs and Budget

With your timeline clear, it’s time to focus on your healthcare priorities and budget. Start by listing any ongoing medical conditions, necessary prescriptions, and the doctors or specialists you want to continue seeing. This will help you identify plans that meet your specific needs.

Your income is a key factor in determining costs. Marketplace savings are calculated based on your total household income for the entire calendar year - not just what you’re earning while unemployed. Be as precise as possible when estimating your income. If you underestimate, you may have to repay some or all of the premium tax credits when you file taxes. For reference, in 2026, a job-based plan (like one through a spouse) is considered "affordable" if the employee’s share of the monthly premium is less than 9.96% of household income.

Think about how often you use healthcare services. If you rarely visit the doctor and mainly need emergency coverage, a high-deductible plan with lower monthly premiums might be a good fit. On the other hand, if you have frequent medical appointments or take several prescriptions, a higher-tier plan with more comprehensive coverage could save you money over time.

Before finalizing any plan, call your preferred doctors to confirm they're in-network and review the plan’s prescription formulary to understand the costs of your medications.

Step 2: Review COBRA Continuation Coverage

COBRA, short for the Consolidated Omnibus Budget Reconciliation Act, allows you to temporarily continue your employer-sponsored health insurance after losing your job. It’s a way to maintain your existing network of doctors and benefits without interruption.

COBRA Eligibility and Enrollment Deadlines

After assessing your coverage needs, COBRA might be a viable option. It’s available if your employer has at least 20 employees or if you're covered under a state or local government plan. If your employer is smaller, check with your state insurance commissioner about "mini-COBRA" laws that might apply.

You have 60 days to enroll in COBRA after receiving your election notice or losing your coverage. If you miss this window, you lose the option to continue your plan. The good news? COBRA coverage is retroactive to the day your previous insurance ended. After electing COBRA, your first payment must be made within 45 days.

"You have 60 days to enroll in COBRA once your employer-sponsored benefits end. Even if your enrollment is delayed, you will be covered by COBRA starting the day your prior coverage ended." - U.S. Department of Labor

COBRA Costs and Benefits

Once you confirm your eligibility, it’s time to weigh the costs against the benefits. Under COBRA, you’re responsible for the entire premium - both your portion and your employer’s portion - plus a 2% administrative fee. This means you’ll pay up to 102% of the plan’s cost.

For context, in 2024, the average employee paid about $114 per month for individual coverage while working. That same plan under COBRA jumps to over $760 per month. For family coverage, the cost increases from $525 to over $2,173 per month.

To estimate your COBRA premium, check Box 12, Code DD on your most recent W-2 form. This shows the total annual cost of your plan - divide by 12 to get your monthly rate. COBRA coverage typically lasts 18 months after job loss, but certain events like divorce or the death of the covered employee can extend it to 36 months.

The main advantage of COBRA? You keep the exact same coverage you had while employed. That means no changes to your doctors, benefits, or prescriptions. Plus, if you’ve already made progress toward your deductible or out-of-pocket maximum, that progress carries over. During severance negotiations, it’s worth asking if your employer can cover part of your COBRA premiums for a few months.

Understanding COBRA’s details helps you decide if it’s the best option or if exploring marketplace and public plan alternatives makes more sense for your situation.

Step 3: Apply for Marketplace Health Insurance Plans

If COBRA doesn't meet your needs, the Health Insurance Marketplace is another option to maintain your coverage. Managed federally through HealthCare.gov and also through state platforms, the Marketplace lets you explore and sign up for health insurance plans.

How to Apply for a Marketplace Plan

Losing a job - whether you quit, were laid off, or terminated - qualifies you for a Special Enrollment Period (SEP). This gives you 60 days from the date your coverage ends to apply. Miss that window, and you'll have to wait for the next Open Enrollment Period unless you experience another qualifying life event.

The application process is straightforward and involves four key steps:

Create an account on HealthCare.gov or your state’s Marketplace website.

Gather required documents, such as personal details for everyone in your tax household, proof of job-based coverage loss, and income estimates for the year.

Submit your application to determine eligibility.

Select a plan that suits your needs.

Typically, your new coverage will begin on the first day of the month after your job-based insurance ends.

When estimating income for the application, include all sources - such as unemployment benefits, interest, capital gains, and withdrawals from retirement accounts like IRAs or 401(k)s. If your income changes during the year, update your application immediately, as this will affect your eligibility for premium tax credits.

Qualifying for Premium Tax Credits

Once your application is reviewed, you’ll find out if you qualify for premium tax credits, which can help reduce your monthly insurance costs. These credits are subsidies based on your household income. The same application also checks your eligibility for Medicaid and CHIP.

However, if you have access to health insurance through a spouse’s employer, you typically won’t qualify for premium tax credits unless the cost of that plan exceeds 9.96% of your household income in 2026. For instance, if your household income is $50,000 annually, a spouse's plan costing more than $415 per month (calculated as $50,000 × 9.96% ÷ 12) would be deemed unaffordable, potentially making you eligible for Marketplace subsidies.

It’s also worth noting that additional savings introduced during the COVID-19 pandemic ended on December 31, 2025. If you benefited from those savings in prior years, you might see higher premiums in 2026.

All Marketplace plans are required to cover 10 essential health benefits, such as hospitalization, prescription drugs, mental health services, and emergency care. They also cannot deny coverage or charge more based on pre-existing conditions.

Step 4: Check If You Qualify for Medicaid or CHIP

If you've experienced a loss of income after losing your job, it's worth checking if you qualify for Medicaid or CHIP, as they provide free or low-cost health coverage.

Medicaid Eligibility Requirements

Medicaid eligibility depends on factors like income, family size, age, pregnancy status, and disability. In every state, the program offers coverage to low-income children, parents, pregnant women, seniors aged 65 and older, and individuals with disabilities.

In some states, Medicaid is also available to all adults who fall below a specific income level. Even if you're unsure about your eligibility, it's a good idea to apply since state-specific guidelines might still qualify you.

To check if you're eligible, you can apply online. If the Marketplace determines you might qualify, it will forward your information to your state’s Medicaid agency. Alternatively, you can contact your state’s Medicaid office directly. Be prepared with documents like Social Security numbers, proof of income, proof of citizenship or immigration status, and details about your housing costs.

One important feature of Medicaid is its ability to provide retroactive coverage for medical expenses incurred up to three months before enrollment, depending on your income during that period. Additionally, if you were in foster care and received Medicaid on your 18th birthday, you're eligible for coverage until age 26.

How CHIP Covers Children

If your family income is too high for Medicaid but private insurance feels out of reach, your children might qualify for CHIP. CHIP offers health coverage for uninsured children and teens up to age 19.

"The Children's Health Insurance Program (CHIP) is a joint federal and state program that provides health coverage to uninsured children in families with incomes too high to qualify for Medicaid, but too low to afford private or group health plan coverage." - Medicaid.gov

CHIP covers a wide range of services, including routine check-ups, immunizations, doctor visits, prescription medications, dental and vision care, and emergency services. Routine "well child" visits and dental check-ups are completely free. While some states may charge small monthly premiums or copays for other services, families won’t pay more than 5% of their annual income for CHIP-related costs.

You can apply for CHIP at any time, as there’s no enrollment deadline. Applications can be submitted via HealthCare.gov, through your state’s CHIP agency, or by calling 1-800-318-2596. Once approved, your child’s coverage can begin immediately.

After determining your eligibility for Medicaid or CHIP, you’ll be ready to move on to Step 5 and explore individual health insurance options.

Step 5: Get Individual Health Insurance Through United National Healthcare

If COBRA, Marketplace plans, Medicaid, or CHIP don’t quite fit your needs, it’s worth exploring what United National Healthcare has to offer. Their plans are designed with flexibility in mind, catering specifically to those transitioning between jobs. One major advantage? These plans are often less expensive than COBRA, as they don’t include the full cost of your former employer’s premium plus administrative fees. United National Healthcare provides a practical, budget-friendly alternative customized for your situation.

United National Healthcare Plan Features

United National Healthcare offers a variety of plans to suit different needs:

ACA Marketplace Plans: These provide comprehensive benefits, including coverage for pre-existing conditions and potential eligibility for premium tax credits.

Short Term Health Insurance: Ideal for bridging coverage gaps while job hunting. These plans are affordable but typically exclude pre-existing conditions and require medical underwriting.

TriTerm Medical Insurance: Offers nearly three years of continuous coverage, perfect for those needing longer-term protection.

Supplemental Coverage: Add-ons like dental, vision, accident, critical illness, or hospital indemnity insurance can enhance your primary plan.

Most plans include application assistance to simplify the enrollment process. Additionally, many options come with no network restrictions, giving you the freedom to choose your preferred healthcare providers.

Comparing Plan Options and Costs

Your monthly premium will vary based on factors like age, location, and the type of plan you choose. United National Healthcare’s "Find a Doctor" tool can help confirm whether your preferred providers are in-network. Plus, losing your job-based health coverage qualifies as a life event, enabling you to apply during a Special Enrollment Period.

"Losing your health care coverage when you leave your job is a qualifying life event that opens a special enrollment period... Now you can buy your own individual health insurance plan that may be less expensive than your former group plan." - UnitedHealthOne

Considering that it takes an average of 40 weeks to find new employment after a job loss, selecting the right health plan now is crucial. United National Healthcare’s online tools make comparing plans simple, helping you find coverage that balances your healthcare needs and budget. This way, you can maintain continuous protection while focusing on your job search.

Conclusion

Key Takeaways

If your job-based insurance ends, you have a 60-day window to secure new coverage through options like COBRA, Marketplace plans, Medicaid, CHIP, or individual plans from United National Healthcare. COBRA lets you keep your current provider network but comes at 102% of the premium cost. Marketplace plans, on the other hand, may offer savings if you qualify for premium tax credits based on your income. Medicaid and CHIP provide year-round enrollment for those with lower incomes.

The best choice depends on your healthcare needs and budget. If keeping your current doctors or prescriptions is non-negotiable, COBRA might justify its higher cost. For lower premiums, Marketplace plans or Medicaid could be a better fit if you meet the income requirements. If you're looking for flexible and often more affordable options, United National Healthcare offers plans tailored for people between jobs, which could cost less than COBRA. Act quickly to ensure you have coverage in place without a gap.

Next Steps for Getting Coverage

Submit your Marketplace application as soon as possible to avoid waiting for the next Open Enrollment Period (November 1–January 15). Confirm the exact end date of your employer-sponsored coverage so you can accurately track your enrollment window. Even if you're unsure about affordability, apply to see if you qualify for subsidies.

If your income changes, update your Marketplace application immediately to adjust your tax credits and avoid surprises at tax time. United National Healthcare offers online tools and application assistance to help you compare plans and find coverage that works for your needs and budget. Taking action now ensures you’ll have the health insurance you need while you focus on your next career move.

FAQs

-

When your job-based health insurance ends, it typically stops either on your last day of employment or on a specific date set by your employer. Once coverage ends, you have a 60-day window to explore other health insurance options like COBRA or Marketplace plans. It’s crucial to check the deadlines and eligibility requirements to ensure you don’t experience any gaps in your coverage

-

Yes, you can move from COBRA to a Marketplace plan without losing coverage - if you act within the right timeframes. You have 60 days after losing your job-based coverage to enroll in a Marketplace plan. However, if you decide to end COBRA early, you'll typically need to wait for the next Open Enrollment period, unless you're eligible for a Special Enrollment Period. To avoid any coverage gaps, make sure to enroll within 60 days of your COBRA coverage ending.

-

When applying for Marketplace subsidies, you’ll need to report your estimated household income for the year. Your eligibility and potential savings depend on this estimate and the size of your household - not your current job status. To ensure you qualify for the right subsidy amount, aim to provide the most accurate annual income estimate possible.