Health Insurance for Gig Workers: Uber, DoorDash, and Amazon Flex Drivers

If you're a gig worker for Uber,DoorDash, orAmazon Flex, securing health insurance can feel like a challenge. Unlike traditional employees, gig workers are independent contractors and don't receive employer-sponsored health benefits. This means you're responsible for finding and managing your own health coverage, which can be tricky with fluctuating income. Here's the good news: affordable options are available, and with the right approach, you can protect yourself financially and medically.

Key Takeaways:

ACA Marketplace Plans: Over 93% of enrollees qualify for subsidies, reducing premiums to around $50/month for many.

Medicaid: Offers free or low-cost coverage if your income is below state-specific limits, often evaluated monthly.

High-Deductible Health Plans (HDHPs) + HSAs: Great for healthy individuals; save on taxes while building a medical fund.

Short-Term Plans: Temporary coverage for gaps but limited benefits and no coverage for pre-existing conditions.

Income Tip: Gig workers with unpredictable earnings should update their ACA Marketplace income estimates frequently to avoid surprises at tax time. You can also lower your taxable income (and potentially increase subsidies) by contributing to a SEP-IRA or HSA.

Why It Matters: Medical bills remain the top cause of bankruptcy in the U.S., making health insurance essential for financial stability. Whether you're a full-time driver or part-time delivery worker, there are options to fit your budget and lifestyle.

Health Insurance Challenges for Gig Workers

When you're out delivering food or driving passengers, you're considered an independent contractor, not an employee. That classification brings more than just tricky tax forms - it leaves you to figure out health insurance entirely on your own. There's no HR department to guide you through enrollment, no group plans to lower costs, and no workers' compensation if you get injured on the job.

While full-time employees often benefit from employer-supported health coverage, gig workers must foot the entire bill (minus any subsidies from the Affordable Care Act, or ACA). You're responsible for managing all the paperwork, estimating subsidies, and covering 100% of your premiums - something W-2 employees usually split with their employer.

Gig Workers vs Traditional Employees: A Comparison

The divide between gig workers and traditional employees extends far beyond health insurance. Here's a snapshot of the differences:

| Feature | Gig Workers (Independent Contractors) | Traditional Employees |

|---|---|---|

| Insurance Access | 40% have access through work | 82% have access through work |

| Workers' Comp | Rarely provided | Legally required for most employees |

| Premium Responsibility | 100% (minus ACA subsidies) | Typically shared with employer |

| Income Stability | Fluctuates with demand/hours | Generally fixed salary or hourly |

If you get injured while working, you're often left covering your own medical expenses. A U.S. Labor Department rule, effective March 2024, aims to reduce worker misclassification, potentially shifting more gig workers into traditional employee roles with benefits. But for now, most drivers and delivery workers remain independent contractors.

These challenges are compounded by the unpredictable nature of gig work income, making it even harder to manage insurance costs.

How Variable Income Affects Insurance Costs

The inconsistent earnings common in gig work directly affect ACA subsidy calculations. The real hurdle isn't just finding coverage - it's predicting your annual income. ACA Marketplace subsidies are tied to your estimated earnings, and getting that estimate wrong can have serious financial consequences. If you underestimate, you'll owe money during tax season. Overestimate, and you'll pay higher premiums upfront when cash flow might already be tight.

One week you might earn $500, and the next, $2,000 - especially if you're working peak hours that pay up to 50% more than off-peak times. This kind of income volatility makes accurate projections nearly impossible. To avoid surprises, update your Marketplace application as soon as your earnings change significantly. Staying on top of this helps keep your subsidies aligned and prevents unpleasant surprises during tax reconciliation.

Another strategy? Lower your Modified Adjusted Gross Income (MAGI) by contributing to a SEP-IRA. You can contribute up to 25% of your net self-employment income, with a cap of $69,000 for 2026. This not only helps with retirement savings but also increases your subsidy eligibility.

Health Insurance Options for Gig Workers

Navigating health insurance as a gig worker can feel overwhelming, especially with unpredictable income and no employer-provided benefits. Finding the right plan means balancing costs, coverage, and flexibility. Let’s explore some popular options and how they might work for you.

The ACA Marketplace is a go-to choice for many gig workers. Why? Over 93% of Marketplace enrollees qualify for premium tax credits, which can reduce average monthly premiums to about $50 by 2026. These plans cover pre-existing conditions and provide year-round protection - important when your work takes you on the road or your income fluctuates.

For those with lower or inconsistent earnings, Medicaid offers affordable or even free coverage. Eligibility depends on where you live, but it generally applies to individuals earning less than $20,000 annually. Even better, Medicaid often evaluates eligibility based on monthly income. This means you might qualify during slower months, even if your total yearly income is higher.

High-Deductible Health Plans (HDHPs) with Health Savings Accounts (HSAs) are another option, especially if you’re healthy and want to save for the future. These plans have lower monthly premiums but higher upfront costs for care. The HSA adds a saving and tax advantage: contributions lower your taxable income, funds grow tax-free, and withdrawals for medical expenses are tax-free too. Christine Corsini, a Personal Benefits Manager at HSA for America, emphasizes the benefits:

Every dollar you contribute [to an HSA] reduces your taxable income... No other savings account offers all three [tax] benefits.

In 2026, HSA contribution limits will be $4,400 for individuals and $8,750 for families, with an extra $1,000 catch-up contribution for those 55 and older. Providers like United National Healthcare allow you to customize HDHPs, tailoring coverage and premiums to your needs.

ACA Marketplace Plans: Affordable Coverage with Subsidies

ACA Marketplace plans base costs on your Modified Adjusted Gross Income (MAGI) - your total income minus certain deductions. Subsidy eligibility in 2026 will generally range from 100% to 400% of the federal poverty level, as enhanced subsidies are set to end in 2025. Keeping track of your 1099 income and deducting expenses like mileage ($0.70/mile in 2026), supplies, and phone costs can lower your MAGI and increase your chances of qualifying for subsidies.

However, estimating your income can be tricky. If you underestimate, you might owe money at tax time. Overestimating could mean higher premiums when money is tight. If you’re self-employed and show a net profit, you can usually deduct health insurance premiums on your taxes - just not the portion already covered by subsidies.

High-Deductible Health Plans (HDHPs) with HSAs

HDHPs come with higher deductibles - $1,700 for individuals and $3,400 for families in 2026 - but lower monthly premiums. While you’ll pay more upfront for care, the overall savings can be worth it if you don’t visit the doctor often. Pairing an HDHP with an HSA turns your plan into a long-term savings tool. Funds roll over year to year and can even be invested in mutual funds, growing tax-free until you need them for medical expenses. Once you hit 65, you can withdraw HSA funds for non-medical purposes without penalty, though you’ll pay regular income tax.

This setup is ideal if you’re younger, healthy, and looking to save on taxes while building a medical emergency fund. Providers like United National Healthcare offer flexible HDHPs, letting you adjust deductibles and coverage to fit your budget. You can also combine HDHPs with ACA subsidies to further reduce premiums while contributing to your HSA.

Medicaid and State-Sponsored Programs

When income dips, Medicaid can be a lifeline. Unlike ACA plans, Medicaid eligibility often depends on monthly income, not yearly totals. This means a slow month might make you eligible, even if your annual earnings are higher. States that expanded Medicaid under the ACA cover adults earning up to 138% of the federal poverty level - about $20,783 annually for an individual in 2026. Other states may have stricter limits.

For families, the Children’s Health Insurance Program (CHIP) provides coverage for kids in households that earn too much for Medicaid but still struggle with private insurance costs. Medicaid offers comprehensive benefits like coverage for pre-existing conditions, preventive care, emergency services, and prescriptions - all with little to no premiums or copays. The trade-off? A more limited provider network compared to private plans. Still, for gig workers dealing with financial uncertainty, Medicaid offers reliable coverage without a hefty price tag.

Before applying, check your state’s specific Medicaid rules, as eligibility and benefits vary widely. Some states process applications within days, making it a quick solution during financial downturns.

Coverage for Pre-Existing Conditions

If you're a gig worker managing chronic conditions like diabetes, asthma, or high blood pressure, ACA Marketplace plans have you covered. These plans ensure that insurance companies cannot deny coverage, charge higher premiums, or exclude treatments tied to your condition. This protection is a game-changer for gig workers dealing with unpredictable incomes and little to no employer support.

"ACA Marketplace plans cannot deny you or charge more for pre-existing conditions."

Medicaid also provides extensive coverage for pre-existing conditions, often with little to no monthly premiums. Since Medicaid eligibility is based on monthly income, you may qualify during slower earning periods, even if your annual income is higher.

However, be cautious with short-term health insurance and health sharing programs. Short-term plans often exclude coverage for chronic conditions, and health sharing programs typically have long waiting periods before covering related expenses. While these options might seem budget-friendly, they can leave you exposed when you need coverage the most.

To navigate these options, United National Healthcare offers expert support. Their licensed agents can guide you through the ACA Marketplace, helping you estimate your variable income to maximize premium tax credits. With over 93% of Marketplace enrollees qualifying for these credits, many pay around $50 per month for coverage after the credits are applied. If your income changes during the year, updating your Marketplace application promptly ensures your subsidies adjust accordingly, helping you avoid surprises at tax time.

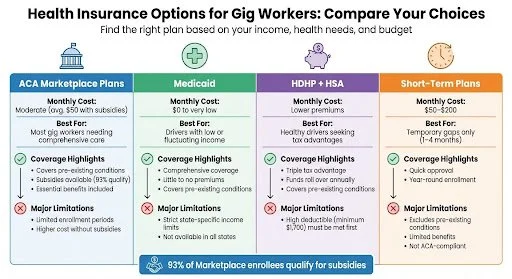

Comparing Insurance Options for Gig Workers

Health Insurance Options for Gig Workers: Cost and Coverage Comparison

Plan Comparison: Marketplace Plans, HDHPs, Medicaid, and Short-Term Plans

Navigating health insurance as a gig worker can feel overwhelming, especially with unpredictable income and a lack of employer-sponsored plans. To make things easier, here's a breakdown of your main options, so you can choose based on your health needs, budget, and income.

ACA Marketplace plans are a solid choice for most gig workers who need broad coverage. The good news? Over 93% of enrollees qualify for premium tax credits, which can bring the average monthly cost down to about $50 during open enrollment. However, enrollment is limited to specific windows - typically from November 1 to January 15 - or if you experience a qualifying life event, like a change in household size or income.

Medicaid can be a lifesaver if your income varies month to month. Eligibility is assessed on a monthly basis, meaning you might qualify during slower months, even if your annual earnings are higher. Coverage is either free or very low-cost. That said, Medicaid availability depends on whether your state has expanded the program, so it’s essential to check your state’s income limits.

High-deductible health plans (HDHPs) with HSAs are ideal for healthy individuals looking to save on taxes. These plans have lower premiums, but you’ll need to meet a deductible of at least $1,700 for individuals or $3,400 for families before the plan starts covering costs. The real perk? The triple tax advantage - contributions are deductible, funds grow tax-free, and withdrawals for medical expenses are tax-free. For 2026, individuals can contribute up to $4,400, while families can contribute up to $8,750 to their HSA. Plus, unused funds roll over, making it a long-term option.

If you’re in between plans, short-term plans might be worth considering. They cost between $50 and $200 per month and are designed for brief coverage periods of one to four months. However, they don’t cover pre-existing conditions or meet ACA standards for essential benefits. Use these only to fill temporary gaps, not as a permanent solution. A licensed agent can help you decide whether a short-term plan or a subsidized Marketplace plan is the better fit.

| Plan Type | Monthly Cost | Best For | Coverage Highlights | Major Limitations |

|---|---|---|---|---|

| ACA Marketplace | Moderate (avg. $50 with subsidies) | Most gig workers needing comprehensive care | Covers pre-existing conditions; subsidies available; essential benefits included | Limited enrollment periods; higher cost without subsidies |

| Medicaid | $0 to very low | Drivers with low or fluctuating income | Comprehensive coverage; little to no premiums; covers pre-existing conditions | Strict state-specific income limits; not available in all states |

| HDHP + HSA | Lower premiums | Healthy drivers seeking tax advantages | Triple tax advantage; funds roll over annually; covers pre-existing conditions | High deductible (minimum $1,700) must be met first |

| Short-Term | $50–$200 | Temporary gaps only (1–4 months) | Quick approval; year-round enrollment | Excludes pre-existing conditions; limited benefits; not ACA-compliant |

Conclusion

Securing health insurance as a gig worker is not only possible but also crucial. When you're running your own business, safeguarding your health is just as important as managing your finances. Medical bills remain the top cause of bankruptcy in the United States, making dependable health coverage a key part of financial security.

Thankfully, affordable options are within reach. Over 93% of Marketplace enrollees qualify for subsidies, often lowering monthly premiums to around $50. This makes health insurance an accessible safety net for both your personal well-being and your business. Whether you choose an ACA Marketplace plan, a high-deductible health plan paired with aHealth Savings Account, Medicaid during slower months, or a short-term plan for temporary coverage, there’s a solution to match your unique financial and health circumstances.

If navigating these choices feels overwhelming, tailored guidance can make the process easier. United National Healthcare offers personalized support to help gig workers and small business owners find the right coverage. Their licensed agents can assist with understanding subsidies, comparing metal tiers, and ensuring your preferred doctors or hospitals are included in your plan. They provide flexible health insurance options designed to meet the diverse needs of freelancers.

"Being your own boss doesn't mean going without health insurance... You have more affordable options than you probably realize." - Christine Corsini, Personal Benefits Manager

To stay ahead, track your income, mark your calendar for open enrollment (November 1 through January 15), and take advantage of preventive care - most plans cover annual checkups at no cost. By acting now, you can secure financial protection and peace of mind, allowing you to focus on growing your business without the added stress of unexpected medical expenses.

FAQs

-

If your gig income varies and you're trying to estimate your income for ACA subsidies, focus on projecting your total earnings for the current year rather than relying on last year’s tax return. Start by calculating your net income - subtract your business expenses from your gross earnings. Don’t forget to include any other income sources, such as investments or side jobs. As your earnings fluctuate, update your estimate to ensure your subsidy eligibility and amounts remain accurate.

-

Yes, it’s possible to move between Medicaid and an ACA Marketplace plan during the year, but you can’t be enrolled in both at the same time. Whether you qualify depends on your income and specific circumstances. If your financial situation changes, you might be eligible to switch plans during open enrollment or a special enrollment period. Take the time to explore your options to maintain uninterrupted coverage.

-

Before choosing a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA), make sure the plan qualifies as HSA-eligible and adheres to IRS rules for deductibles. Evaluate whether it suits your healthcare needs, fits your budget, and covers any pre-existing conditions you may have. Pay close attention to factors like premiums, deductibles, and out-of-pocket maximums. Additionally, confirm that the plan includes access to a reliable provider network to ensure you can receive quality care when needed.